The District Child Tax Credit proposal

Analysis of DC Councilmember Zachary Parker's new legislation.

Contents

The District Child Tax Credit

Example household

Scenario analysis

DC-wide impacts

Context of DC’s tax-benefit system

Conclusion

We thank the

On March 3, 2023, DC Councilmember Zachary Parker, along with eight other councilmembers, introduced the

This report delves into the DCTC, providing an overview of the credit, examples of how households could be affected, scenario analysis for various filer types, and potential impacts on poverty and income inequality. Additionally, the report contextualizes the DCTC within DC’s broader tax-benefit system, highlighting the differences in phase-out structures and eligibility criteria compared to other programs.

The District Child Tax Credit#

The DCTC proposes that, starting in the tax year 2026, eligible filers would receive a refundable credit of up to $500 for each qualifying child, up to a limit of three children. Refundable credits can reduce a filer’s tax liability below zero, effectively functioning as benefits paid through the tax code, independent of regular tax liability.

Qualifying children are defined as those eligible for the federal Child Tax Credit, which includes children under the age of 17. The bill also proposes reducing the credit by $20 for each $1,000 (or fraction thereof) by which the taxpayer’s adjusted gross income exceeds the threshold amount, with different thresholds for single filers ($100,000) and joint returns ($145,000). A taxpayer is ineligible to receive this credit if they do not claim the eligible child as a dependent on their federal and District income tax returns, if someone else claims the eligible child, or if the taxpayer has not resided in the District of Columbia for at least one year prior to the date of filing.

Example household#

Consider a household with two children, ages 10 and 16, and an adjusted gross income of $110,000. The DCTC would make them eligible for a maximum credit of $1,000 ($500 per child). However, since their income exceeds the threshold amount for single (head of household) filers by $10,000, the credit falls by $200 ($20 for each $1,000, or 2%). Therefore, the household will receive a final credit of $800.

For a single filer with two children, the credit fully phases out if their income reaches $150,000 ($100,000 phase-out threshold + $1,000 credit / 2% phase-out rate = $100,000 + $50,000).

To see how the DCTC would affect your own household,

Note that our calculator does not reflect the limit of three children or the one-year tenure requirement. It also assumes that your household files taxes together, not married filing separately on the same return.

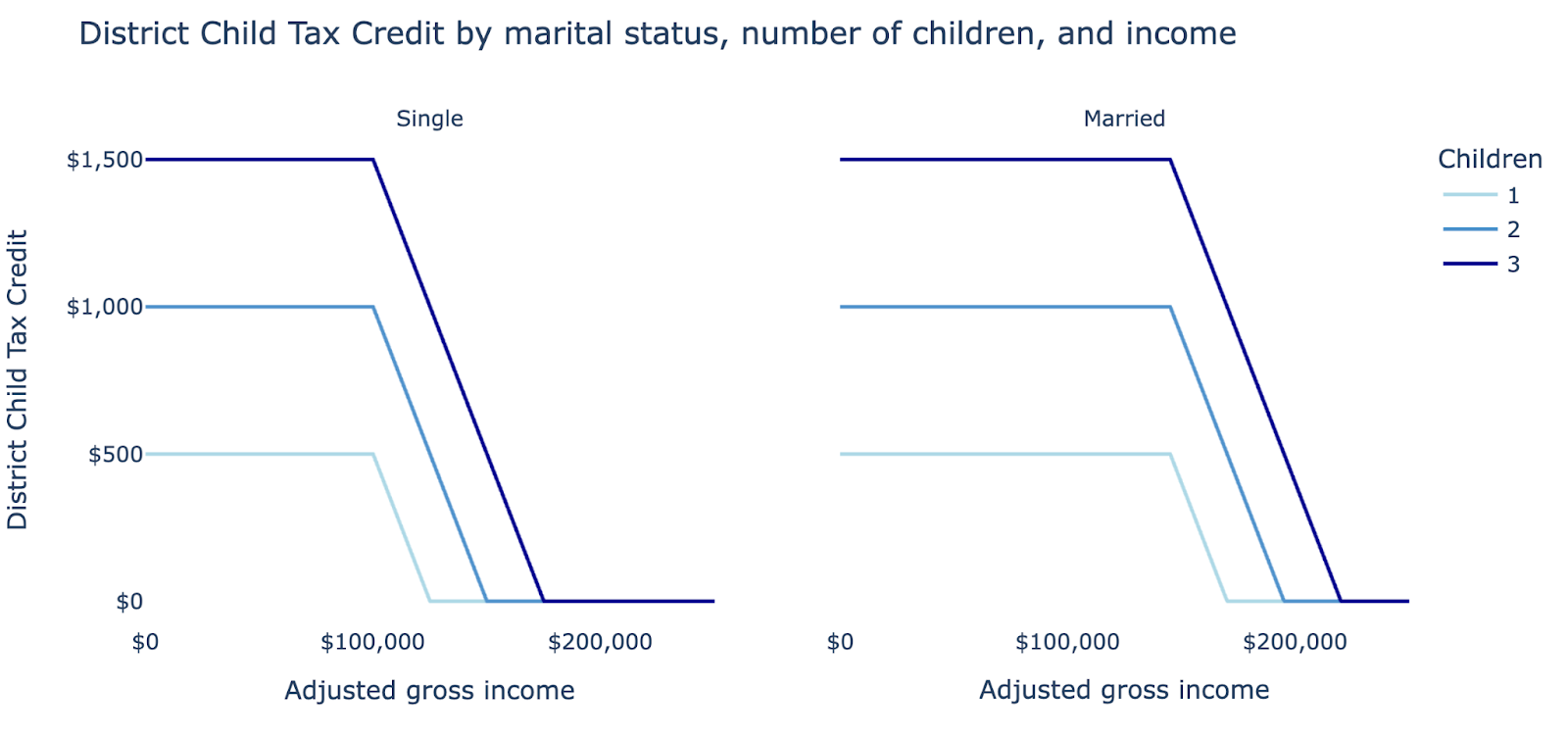

Scenario analysis#

A filer’s DCTC depends on their marital status, number of children, and income, as illustrated in the following chart. Applying similar math to the previous section, the credit fully phases out for single filers with one child at $125,000, two children at $150,000, and three children at $175,000. For married joint filers, the credit fully phases out at $45,000 higher income: $170,000 for one child, $195,000 for two children, and $220,000 for three children.

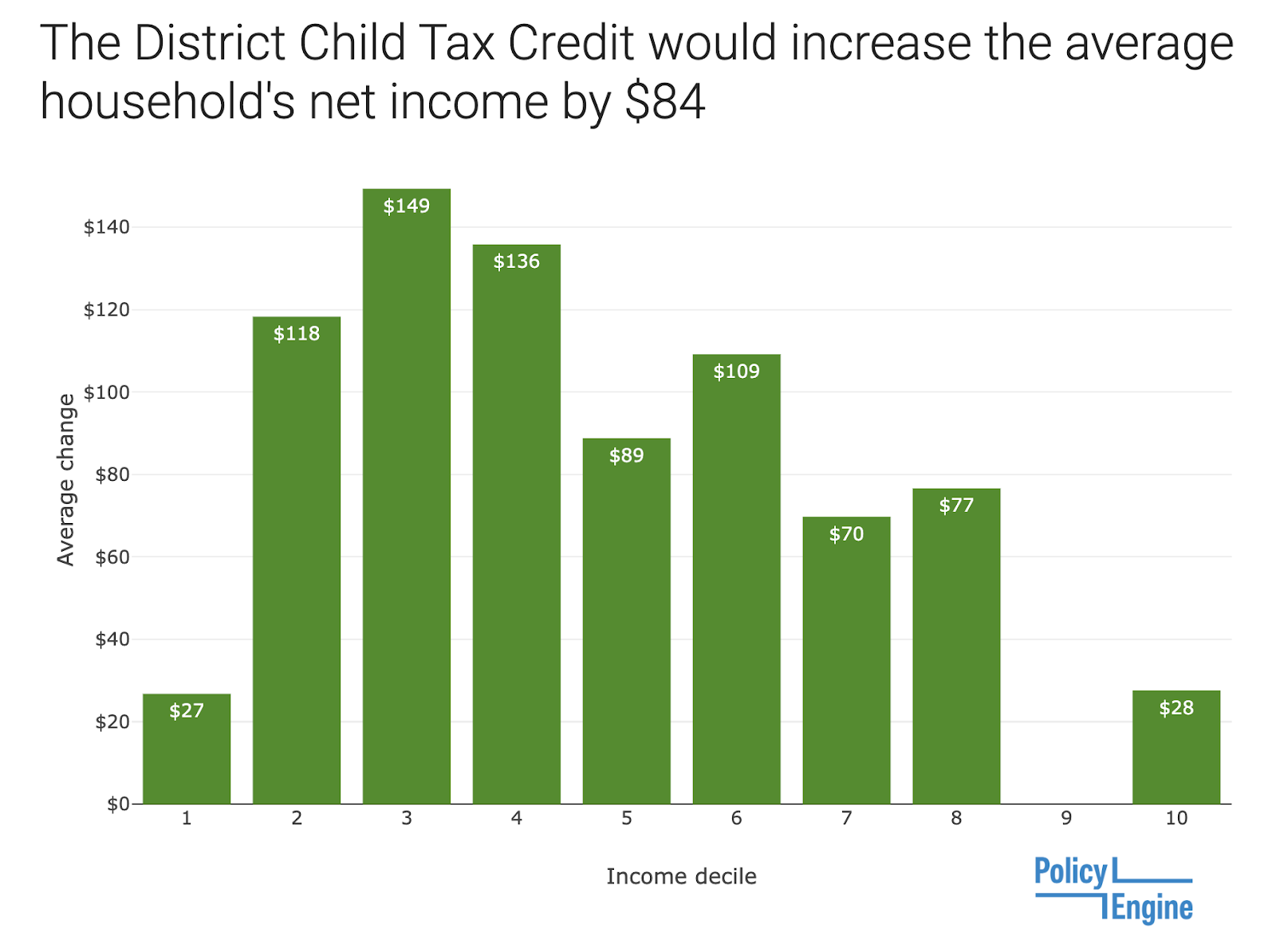

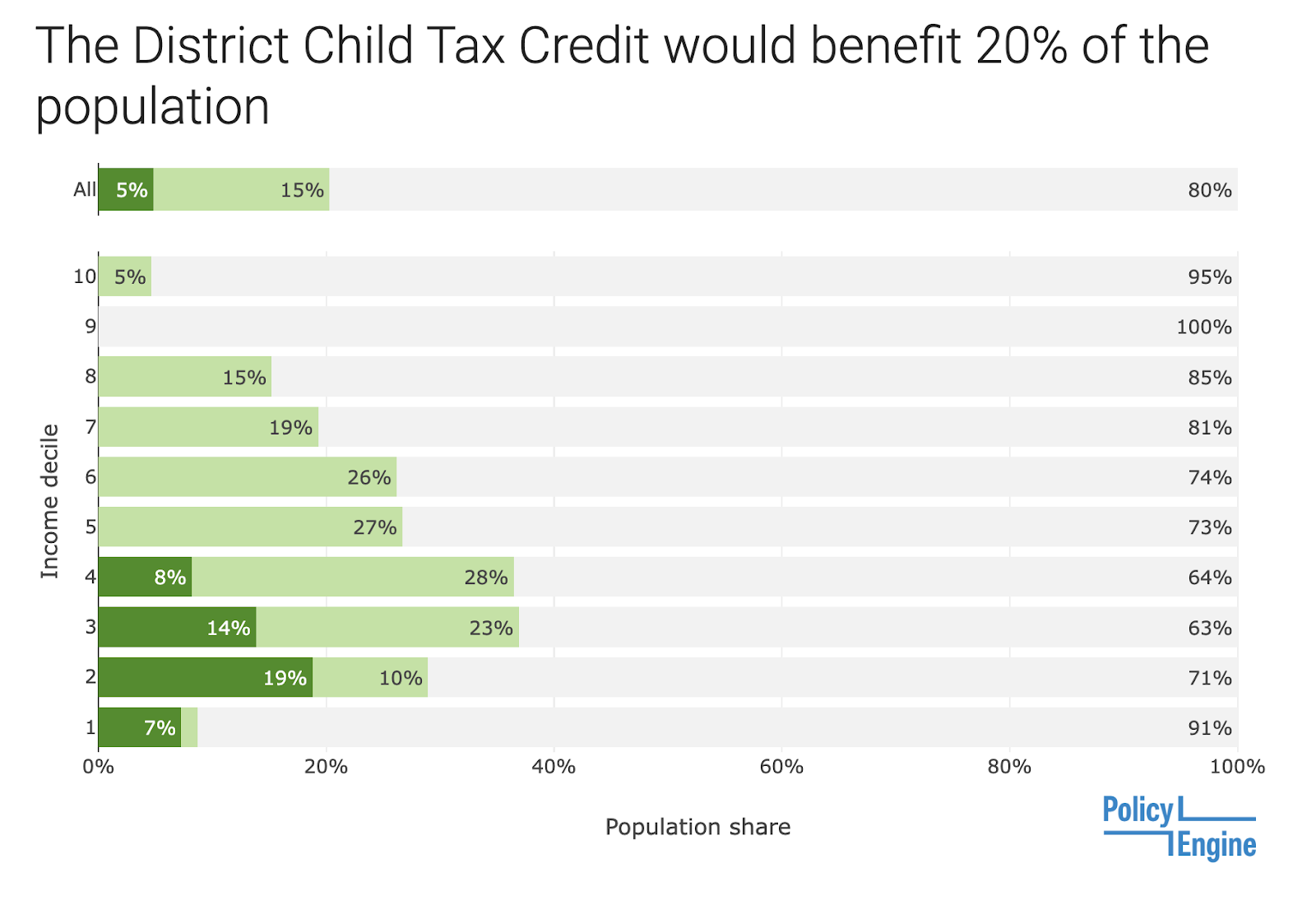

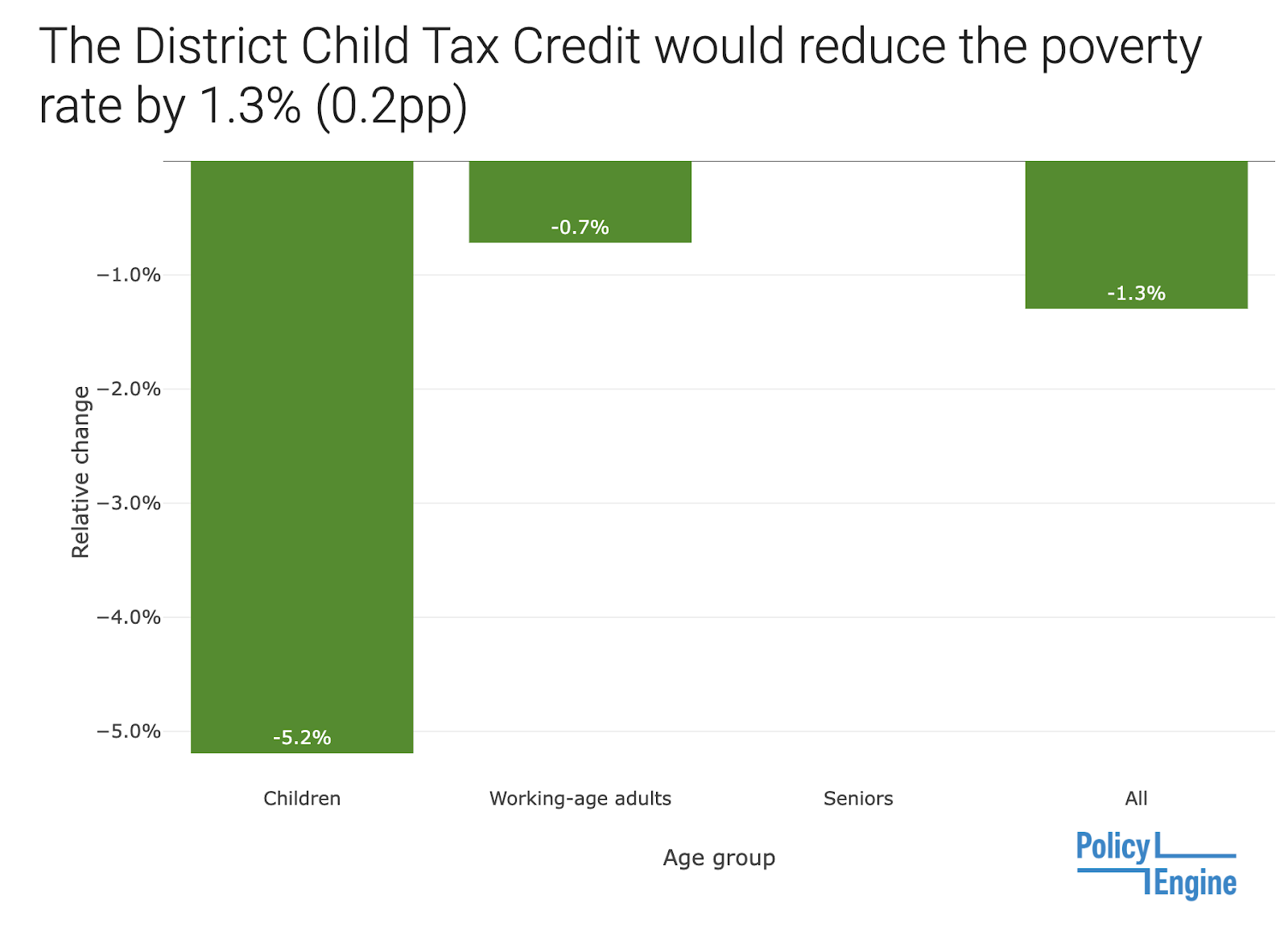

DC-wide impacts#

PolicyEngine estimates population-level impacts by pairing its rules engine with representative survey data released by the US Census Bureau. Specifically, it uses the 2021

PolicyEngine estimates that the DCTC would

The DCTC would

Context of DC’s tax-benefit system#

As a refundable tax credit, the DCTC would effectively serve as a benefit paid through the tax system. Some other refundable tax credits and cash benefits in DC include:

-

DC Earned Income Tax Credit (EITC), which currently matches 70% of the federal EITC and will match 100% beginning in 2026 -

DC Homeowner and Renter Property Tax Credit provides a credit based on property tax or rent paid, age, and income -

DC Keep Child Care Affordable Credit provides a credit based on childcare expenses, children and their ages, and income -

DC Temporary Assistance for Needy Families (TANF), which provides cash assistance to low-income families with children

While PolicyEngine does not yet model these programs for a quantitative comparison, we can describe some ways in which the DCTC diverges from them.

One difference is the phase out structure. The DCTC phases out more slowly and at a higher income than other DC programs: at 2% of income exceeding $100,000 or $145,000. For comparison, the DC EITC for filers with children phases out at 11–15% of income exceeding $21,560.

The DCTC also depends on fewer household characteristics than other programs. The Homeowner and Renter Property Tax Credit depends on rent and property taxes; the Keep Child Care Affordable Credit depends on childcare expenses; TANF depends on assets. The DCTC depends only on children, marital status, and income.

Conclusion#

The District Child Tax Credit Amendment Act of 2023 proposes a refundable credit of up to $500 per child. The program would take effect for the 2026 tax year, issuing its first refunds in early 2027.

Given full take-up, PolicyEngine estimates that it would cost about $27 million, reach 20% of the DC population, reduce child poverty by about 5%, and reduce income inequality by 0.1–0.2%. The design of the DCTC, featuring a gradual phase-out structure and fewer household characteristic dependencies, distinguishes it from other DC programs and may help to mitigate welfare cliffs.

As PolicyEngine continues to refine its model of other DC programs and improve its microdata, the accuracy of estimates for the DCTC’s distributional, budgetary, and incentive effects within the DC public policy environment will also improve. The availability of more data and enhanced capabilities of PolicyEngine could pave the way for future studies, offering additional insights into the potential impact of the DCTC on families in the District of Columbia.

-

The EITC phases out at 15.98% for filers with one child and 21.06% for filers with two or more children. These result in 11–15% when multiplied by DC’s 70% multiplier.

↩

max ghenis

PolicyEngine's Co-founder and CEO

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.