Analysis of the Family First Act

We project that Representative Blake Moore's Child Tax Credit bill would raise revenue and reduce poverty.

Contents

Defining the Reform

Child Tax Credit (CTC)

Pregnant Mother’s Credit

Reform of the Earned Income Tax Credit (EITC)

Repeal of Head of Household Filing Status

Repeal of Dependent Exemptions

Repeal Child Portion of the Child and Dependent Care Credit (CDCC)

Cap the State and Local Tax (SALT) Deduction

Household Impacts of the Family First Act

National Impacts of the Family First Act

Federal Revenue Effects

State Revenue Effects

Changes in Income Distribution

Poverty Reduction

Conclusion

Appendix A: Detailed Policy Comparison

Table A.1: FFA Compared to Current Policy and Current Law (2026)

Appendix B: Simulation Methodology

Data and Software

Key Assumptions

Margin of Error

On January 13th, Congressman Blake Moore (R-UT)

Defining the Reform#

Here we describe each provision of the Family First Act. See Table A.1 in the Appendix for a detailed comparison of FFA, current policy (under TCJA), and current law (post-TCJA).

Child Tax Credit (CTC)#

The FFA expands the CTC from $1,000 to $4,200 for children up to age five and $3,000 for children ages six to 17, up to six children per filer. It phases in from $0 to $20,000 of earnings and phases out at 5% above $200,000 ($400,000 joint), retaining the TCJA thresholds of 2018–2025. Under current law in 2026, the threshold would revert to $75,000 ($110,000 joint).

Pregnant Mother’s Credit#

The FFA adds a pregnant mother’s credit of up to $2,800 for each newborn. It phases in until $10,000 of earnings.

Reform of the Earned Income Tax Credit (EITC)#

The FFA consolidates eight existing EITC household types (single/married and 0/1/2/3+ children) into four (single/married and 0/1+ children). The phase-in rate remains 7.65% for households without children and 34% for those with children. The phase-out rate becomes 10% for households without children and 25% for households with children, compared to 7.65% and up to 21.06% today.

Repeal of Head of Household Filing Status#

The FFA repeals head of household filing status, which increases tax thresholds for single parents under current policy.

Repeal of Dependent Exemptions#

The TCJA repealed dependent exemptions from 2018 to 2025. Starting in 2026, these exemptions would return at $5,300. The FFA continues their repeal, maintaining the TCJA approach.

Repeal Child Portion of the Child and Dependent Care Credit (CDCC)#

The FFA limits the CDCC to dependent care expenses for individuals who are 18 or older and unable to self-care due to disability. Currently, the CDCC is available for children under 13.

Cap the State and Local Tax (SALT) Deduction#

The $10,000 SALT deduction cap from the TCJA is scheduled to expire in 2026. The FFA would keep the $10,000 cap in place.

Household Impacts of the Family First Act#

Consider a single parent with two children, ages five and ten, earning $30,000 in Utah. Under the FFA,

Figure 1 shows how this household's experience

Figure 1: FFA effect on net income for a single parent in Utah with two children ages 5 and 10

Figure 2 shows how the reform

Figure 2: FFA effect on marginal tax rates for a single parent in Utah with two children ages 5 and 10

The reform's effects vary with marital status, number of children, income, and childcare expenses. Figure 3 shows how these factors affect the impact to net income, holding child ages at ages 6 to 12. These impacts differ from those in Figure 1 as they assume (a) all children are age 6 and 12 (rather than 5 and 10), and (b) the household is in Texas, which has no income tax or credits (rather than Utah).

Figure 3: FFA effect on net income by marital status, children, income, and childcare expenses

Single-parent households can see net income decrease by up to $10,000, or more with childcare expenses, with the largest reductions occurring at incomes between $300,000 and $400,000. The magnitude of change increases with the number of children in the household. Married households, in contrast, experience net income increases of up to $4,000-$5,000 until their earnings exceed $400,000. As with single-parent households, those with more children see larger changes in net income due to the expanded Child Tax Credit.

When households have childcare expenses, the impacts shift. A household with $10,000 in childcare expenses sees up to $3,000 less in net income due to changes in the Child and Dependent Care Credit. Married households maintain net gains until reaching about $420,000 in earnings, after which the gains gradually decline. Single households experience a steeper decline in net income as earnings grow, reflecting the reformed EITC structure.

National Impacts of the Family First Act#

We estimate national impacts using the PolicyEngine US microsimulation model. See Appendix B for methodological details.

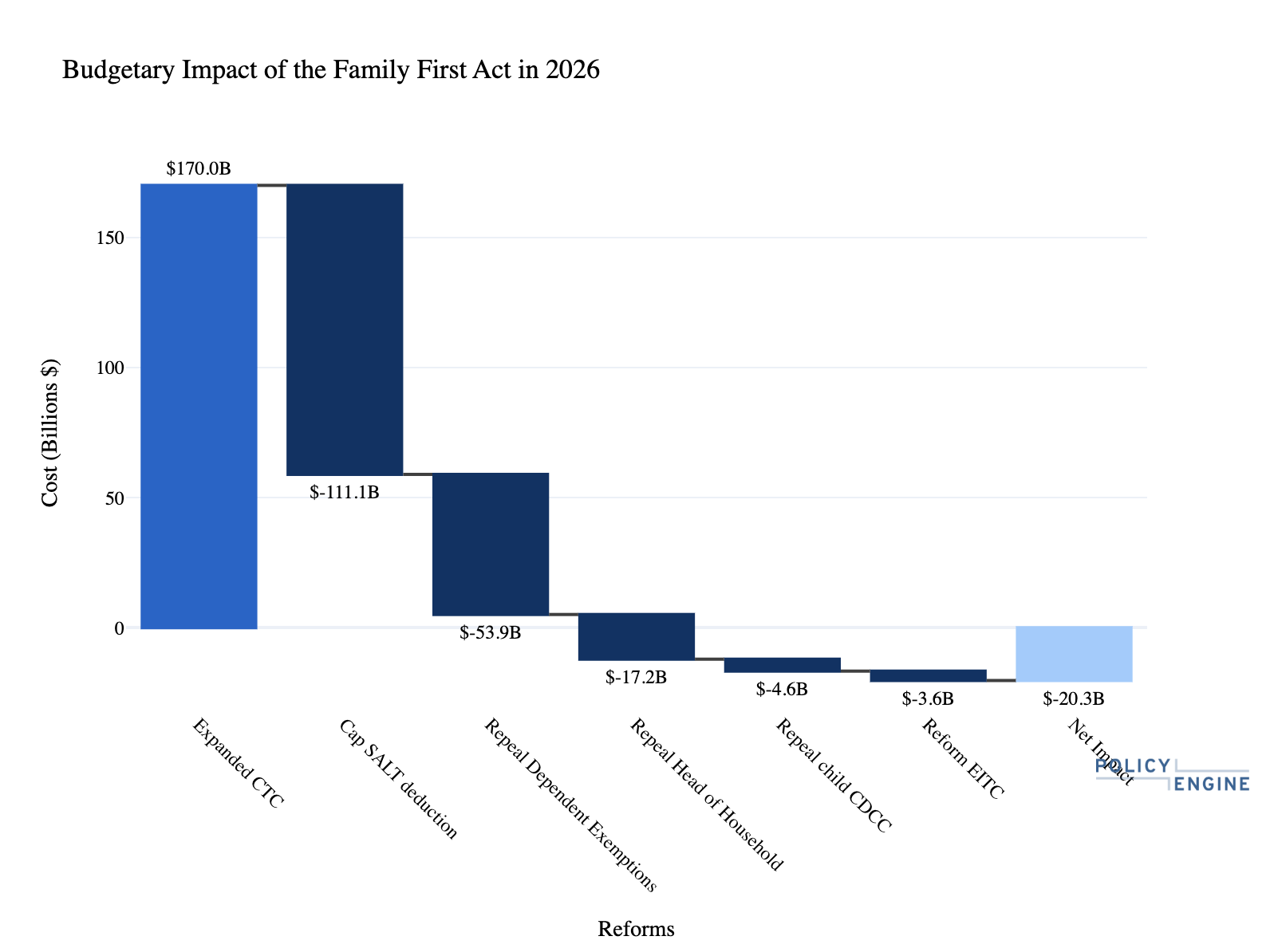

Federal Revenue Effects#

The FFA raises

Figure 4: Federal budgetary impacts of Family First Act provisions in 2026

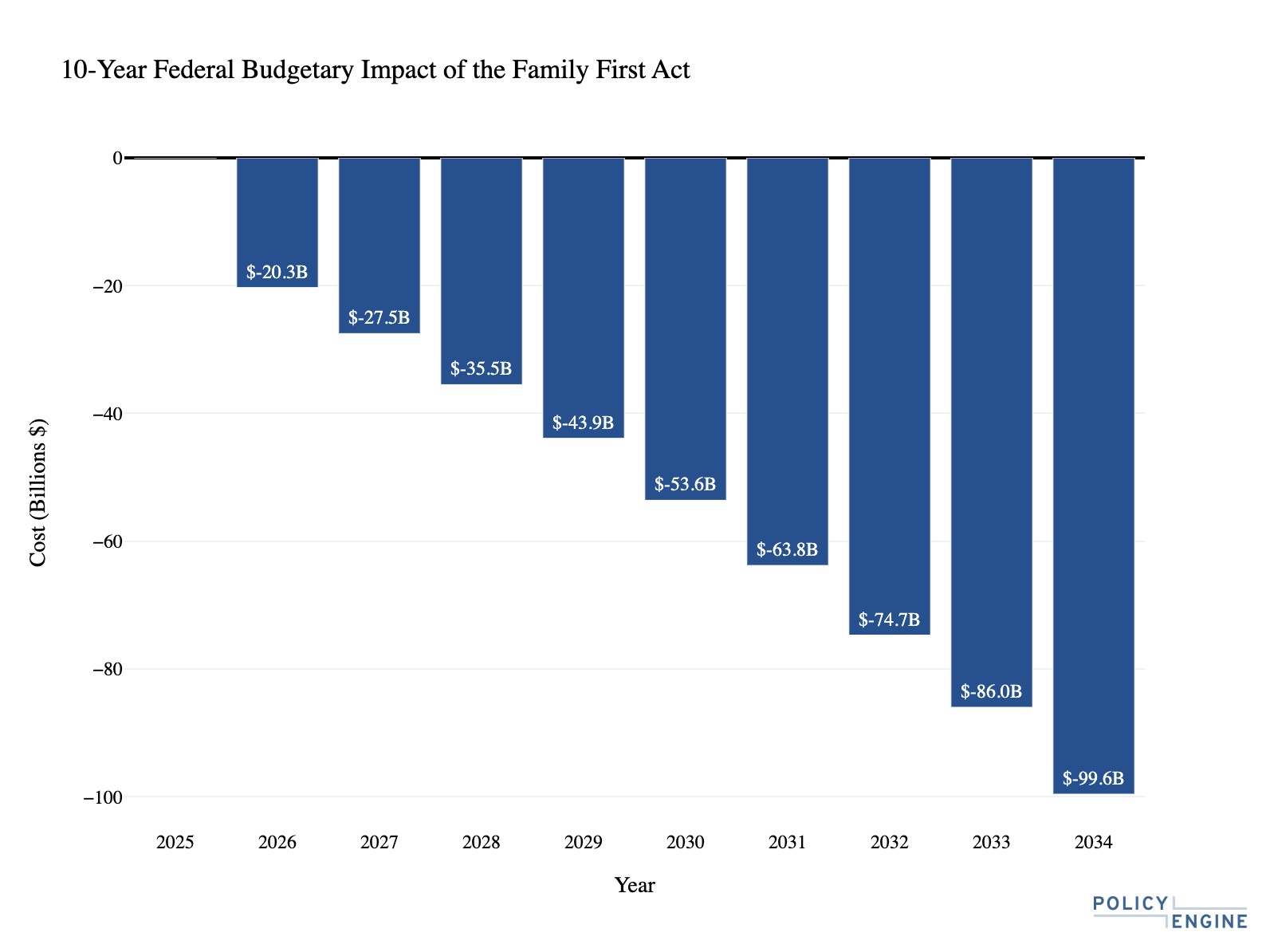

Over the 2025-2034 budget window, the reform raises $505 billion, with federal revenue gains growing each year as shown in Figure 5.

Figure 5: Federal budgetary impacts of Family First Act from 2025 to 2034

State Revenue Effects#

State revenues rise by

Changes in Income Distribution#

The reform affects household incomes across the income distribution, as shown in Figure 6.

Figure 6: Distribution of gains and losses

Poverty Reduction#

The reform

Figure 7: Poverty reduction by age group

The reform also reduces income inequality,

Finally, the reform increases the

Conclusion#

Congressman Blake Moore’s Family First Act modifies multiple tax policies. The bill changes the Earned Income Tax Credit, Child Tax Credit, Child and Dependent Care Credit, and SALT deduction, and it repeals head of household filing status and dependent exemptions. We project that these reforms would raise $505 billion in federal revenues from 2026 to 2034, with the amount increasing annually. According to our simulation, the reform raises net income for 36% of the population and reduces poverty by 5.9% (and child poverty by 10.7%).

Appendix A: Detailed Policy Comparison#

Table A.1: FFA Compared to Current Policy and Current Law (2026)#

Appendix B: Simulation Methodology#

Data and Software#

This analysis uses:

- PolicyEngine US version 1.172.0 microsimulation model

- Enhanced Current Population Survey microdata

- 2026 tax parameters from current law

This specialized code

Key Assumptions#

The simulation:

- Compares FFA to current law baseline after TCJA expiration

- Assumes no behavioral responses to policy changes

- Models full CTC takeup

- Models partial EITC takeup based on

IRS Taxpayer Advocate Service estimates - Includes state tax interactions where credits match federal amounts; distributional impacts consider state impacts, while budgetary impacts break out federal from state

- Projects parameters forward using statutory inflation adjustments and CBO inflation forecasts

Margin of Error#

Results are point estimates from survey microdata. Sampling error and modeling uncertainty affect precision. Key sources of uncertainty include:

- CPS sampling variation

- Income and demographic reporting error

- Tax filing unit construction from households

- Benefit takeup assumptions

- Economic projection uncertainty

- Behavioral responses

pavel makarchuk

Economist at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.