The Family Income Supplemental Credit (FISC) Act

Representative Jared Golden’s Child Tax Credit reform would cost $193 billion in 2026 while reducing poverty and inequality.

Contents

Background

Household Impacts

National Impacts

Poverty Impact

Conclusion

The

PolicyEngine projects that in 2026, the FISC Act would:

-

Reduce federal tax revenue by $193 billion

-

Increase net income for 37% of US residents

-

Lower the Supplemental Poverty Measure by 9.2% and child poverty by 17.7%

Background#

The FISC Act would create a new refundable family income supplement credit with the following structure:

-

A monthly base credit amount of $400 per child under six or $250 per child over six or under eighteen years of age

-

An additional monthly $400 for pregnant mothers after the first five pregnancy months

-

A 20% marriage bonus, which is applied to the total monthly credit amount

The credit phases in linearly with earnings and phases out monthly by $16.67 for each $1,000 increment of adjusted gross income over $125,000 ($250,000 for joint filers).

This new credit’s cost is partially offset by the repeal of the existing Child Tax Credit.

Household Impacts#

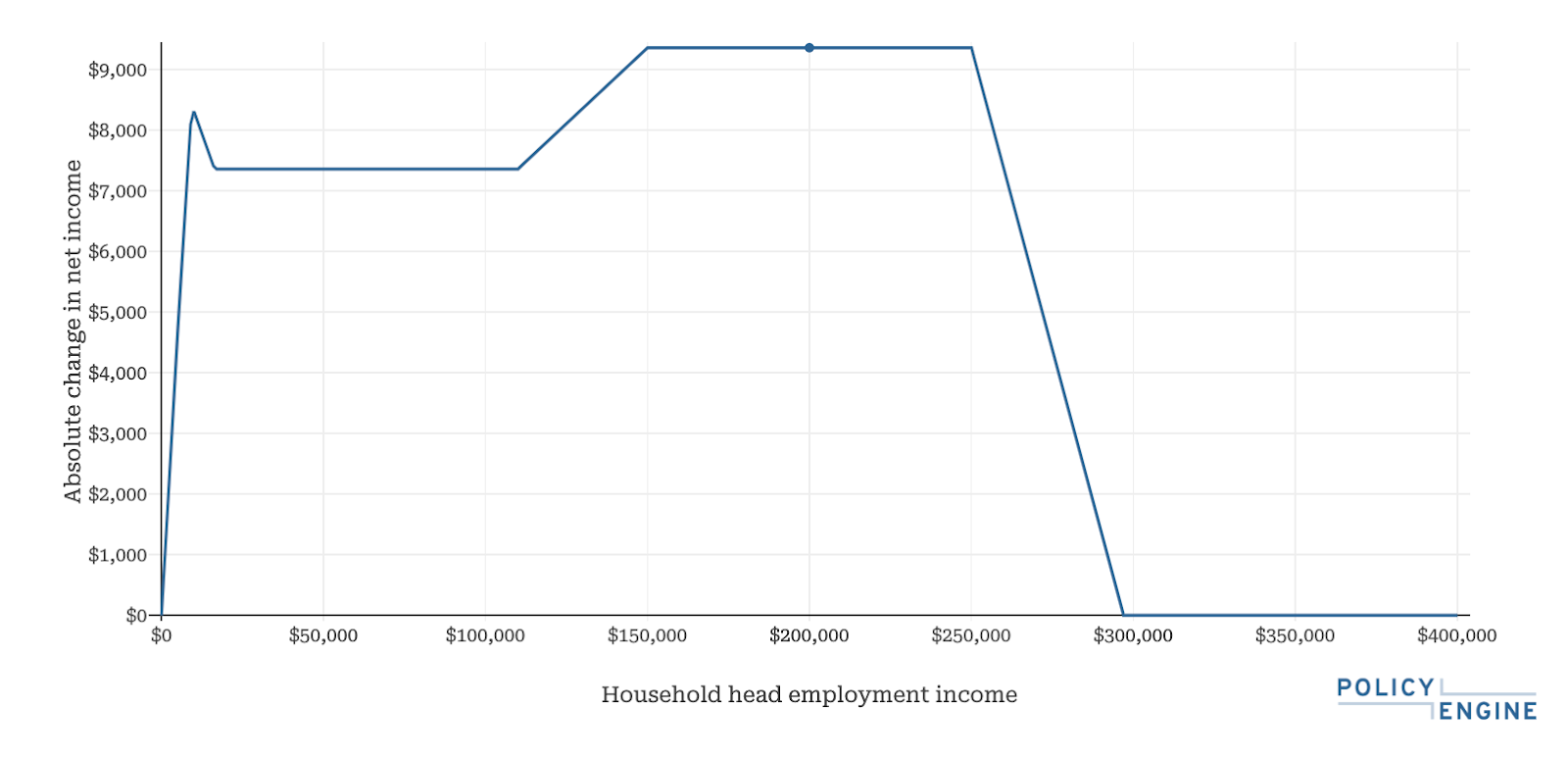

Considering a married couple in Virginia with $40,000 of earnings and two children aged 3 and 10. Under the FISC Act,

Figure 1 shows how this household’s experience

Figure 1: Household Net Income Impact of the FISC Act by Household Earnings

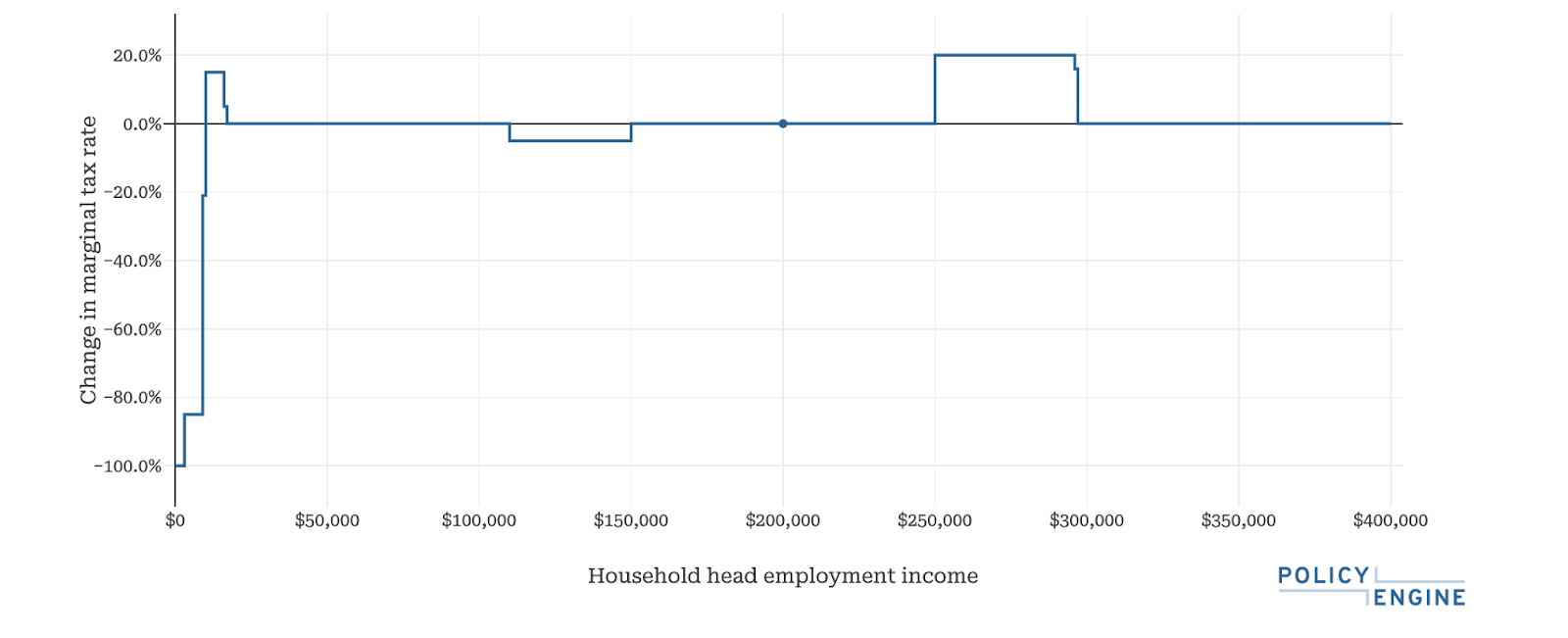

Figure 2. shows how the FISC Act alters the household’s marginal tax rates, with the steeper phase-in structure being reflected in the earnings up to $17,000.

Figure 2: Change in Marginal Tax Rates based on Household Earnings

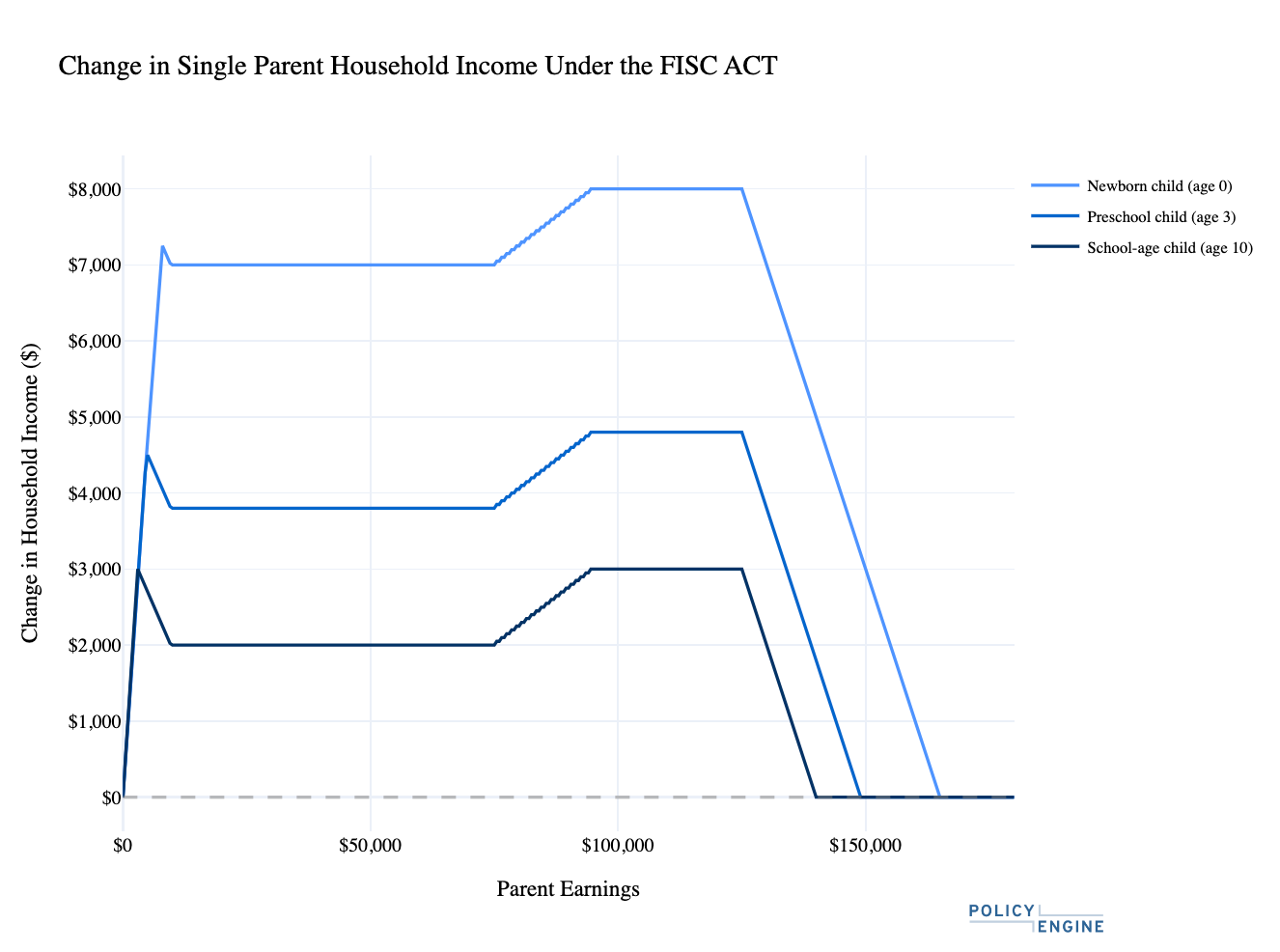

The new credit amount varies with children’s ages while adding an additional pregnancy credit amount. Figure 3 shows the impacts of this credit on net income of a single parent with one child of varying ages. We currently lump four months of the $400 pregnancy credit in with 12 months of the $400 base credit for parents of newborns, applying the full $6,400 in the same year, though we

Figure 3: Change in Household Net Income Under the FISC Act based on Child Ages

National Impacts#

Using PolicyEngine’s microsimulation capabilities, and assuming no behavioral responses, we estimate the national impacts of the FISC Act in the 2026 fiscal year.

The FISC Act would reduce federal revenues by

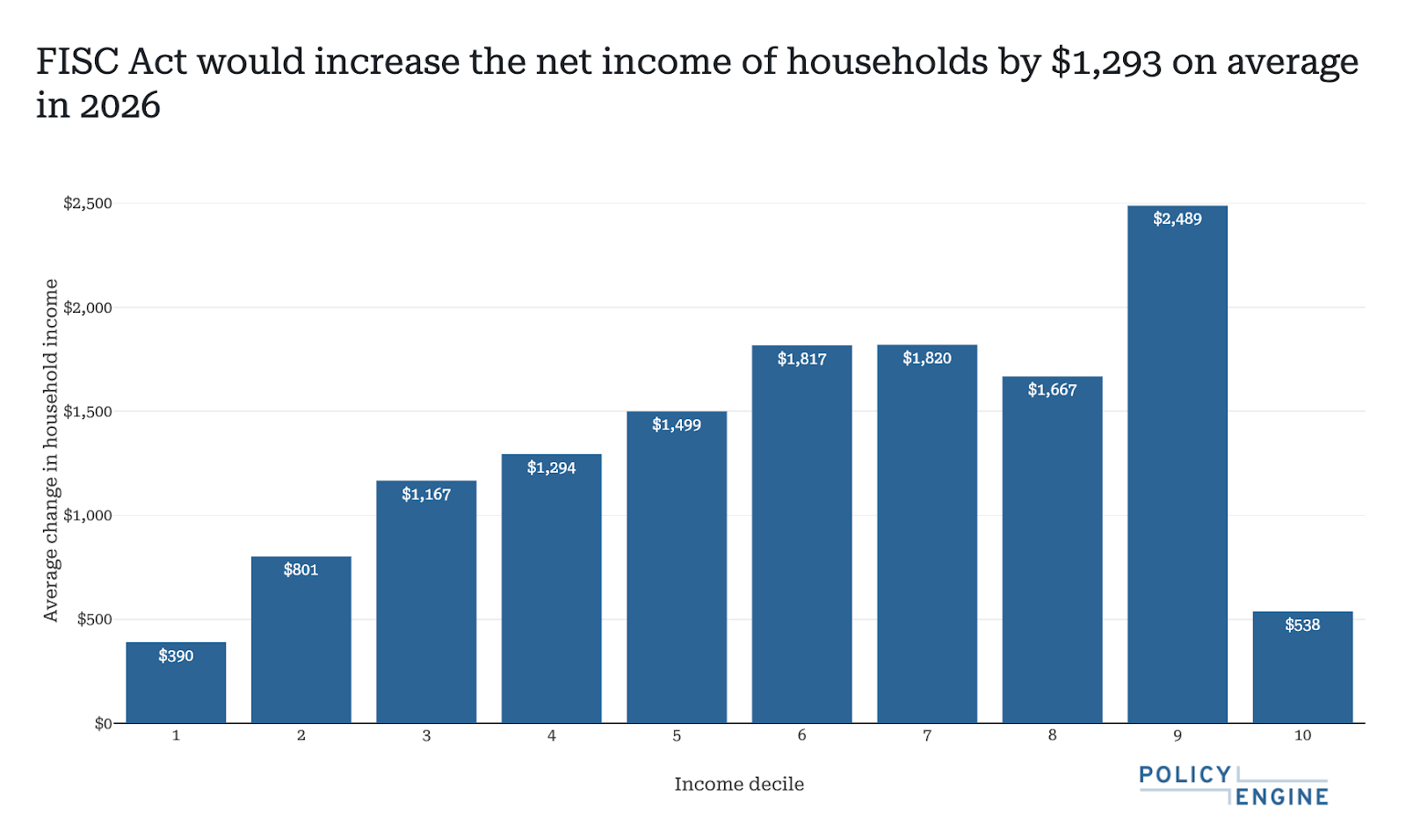

Figure 4: Average Change in Net Income by Income Decile in 2026

Table 1: 10-Year Budgetary Impact of the FISC Act

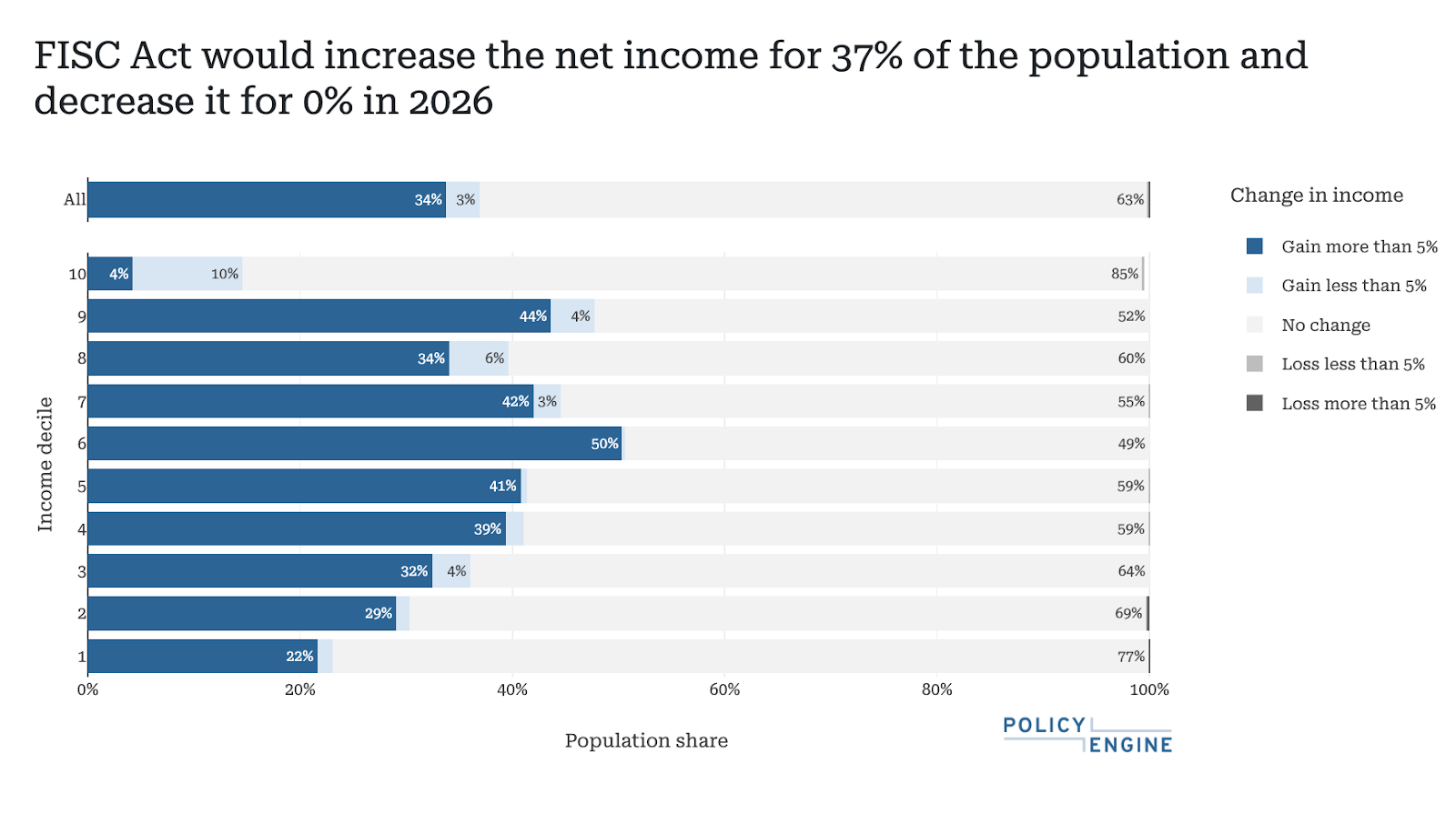

37% of US residents would gain: 50% of those in the sixth decile and 14% of those in the upper decile representing the extrema.

Figure 5: Winners and Losers of the FISC Act in 2026

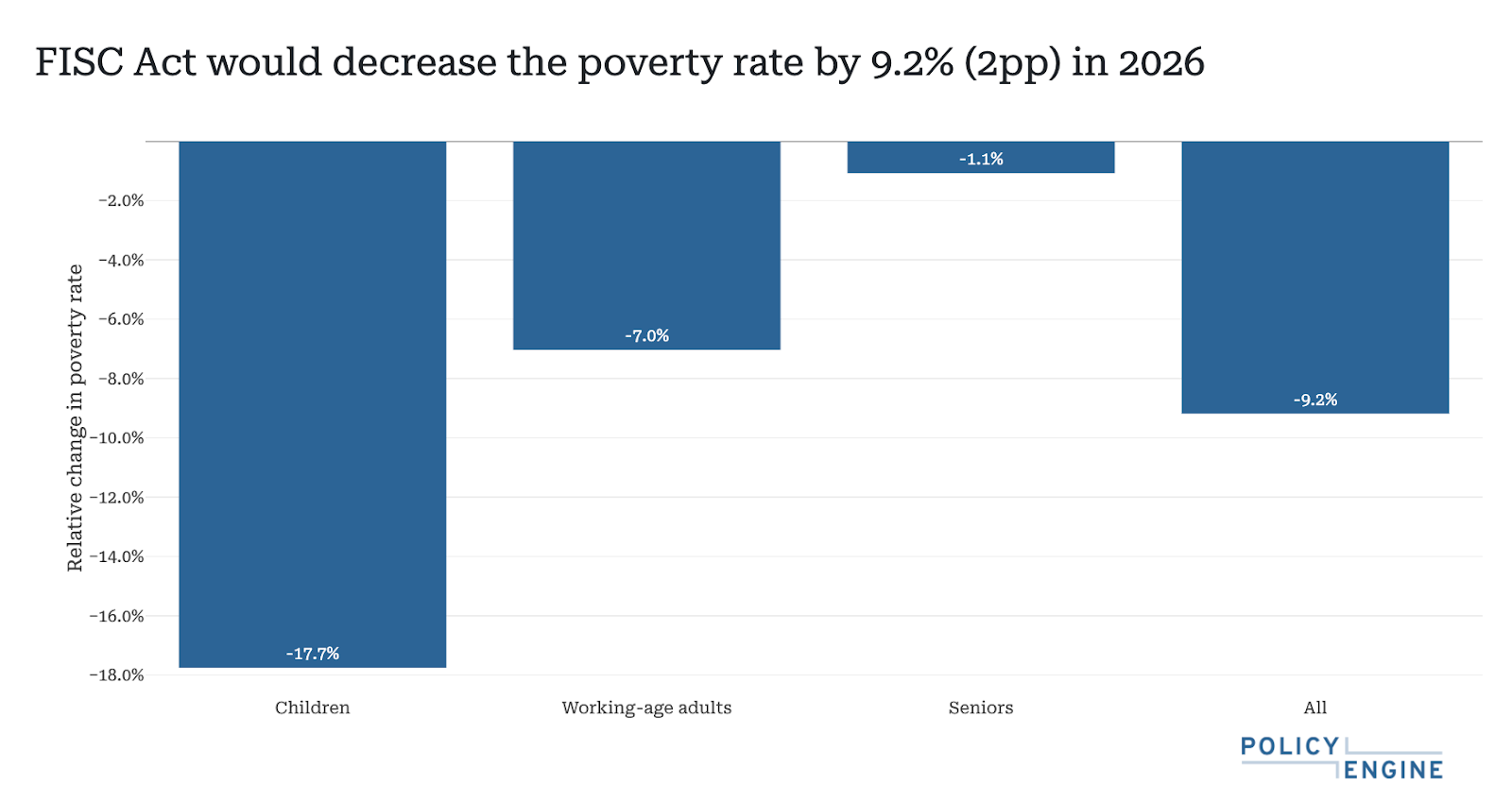

Poverty Impact#

The FISC Act would lower the nation’s Supplemental Poverty Measure by

Figure 6: Poverty Impact of the FISC Act in 2026

Conclusion#

Representative Golden’s FISC Act would replace the Child Tax Credit with a larger credit that varies with child age and marital status, and introduce a pregnancy credit. It would cost $193 billion in 2026, providing larger benefits to households in the middle of the income distribution than those in the top or bottom deciles. Without considering behavioral responses, it would reduce poverty and

To explore how this policy would affect your household or to design your own reform, visit

pavel makarchuk

Economist at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.