Kansas's Flat Tax Proposal — SB169

We review how the bill works and model its impact with PolicyEngine US.

Contents

How would SB169 change Kansas’s tax system, and how much does PolicyEngine model?

How would SB169 affect individual households?

How would SB169 affect Kansas as a whole?

Following the

This post examines the details of these reforms and

How would SB169 change Kansas’s tax system, and how much does PolicyEngine model?#

SB169 would enact nine changes to the tax system. Below we list them, and also note the extent to which PolicyEngine models them.

-

Flatten the current graduated-rate income tax, which currently reaches 5.7%, to 5.25% on income above $5,225 (single) and $12,300 (joint). Fully modeled.

-

Increase the standard deduction for single filers from $3,500 to $4,000. Fully modeled.

-

Inflation-adjust the standard deduction in future years for all filers. Not applicable to PolicyEngine’s one-year model.

-

Eliminate the nonrefundable Food Sales Tax credit, which would otherwise end in 2025. Fully modeled.

-

Eliminate the sales tax on unprepared food. PolicyEngine does not model sales taxes. Note however that food purchased with Supplemental Nutrition Assistance Program benefits (food stamps) are already

exempt from sales taxes . -

Expand the income tax exemption for Social Security benefits: Under current law, Kansans whose total adjusted gross income is $75,000 or less are exempt from taxes on their social security benefits, while those above this threshold are fully taxed. Instead, SB169 would gradually phase out the subtraction for Social Security benefits between $75,000 and $100,000 of adjusted gross income. PolicyEngine models the existing exemption, but this reform amends the structure of the exemption in a way that the app cannot model. We therefore exclude it from this analysis, though invite analysts to model it in our Python package.

-

Decrease the normal tax rate for corporations. Not modeled.

-

Raise the exemption ceiling for residential property taxes. Not modeled.

-

Reduce the tax rate on banks. Not modeled.

PolicyEngine’s limitations may result in our understating the net income benefits to Kansans and the state revenue losses from implementing SB169. Beyond the policies we do not model, our reliance on the Current Population Survey creates inaccuracies that we

How would SB169 affect individual households?#

To explore the effect of SB169 on individuals, we will examine three different sample households: a single 55-year-old, a family of four, and a 70-year-old who receives Social Security.

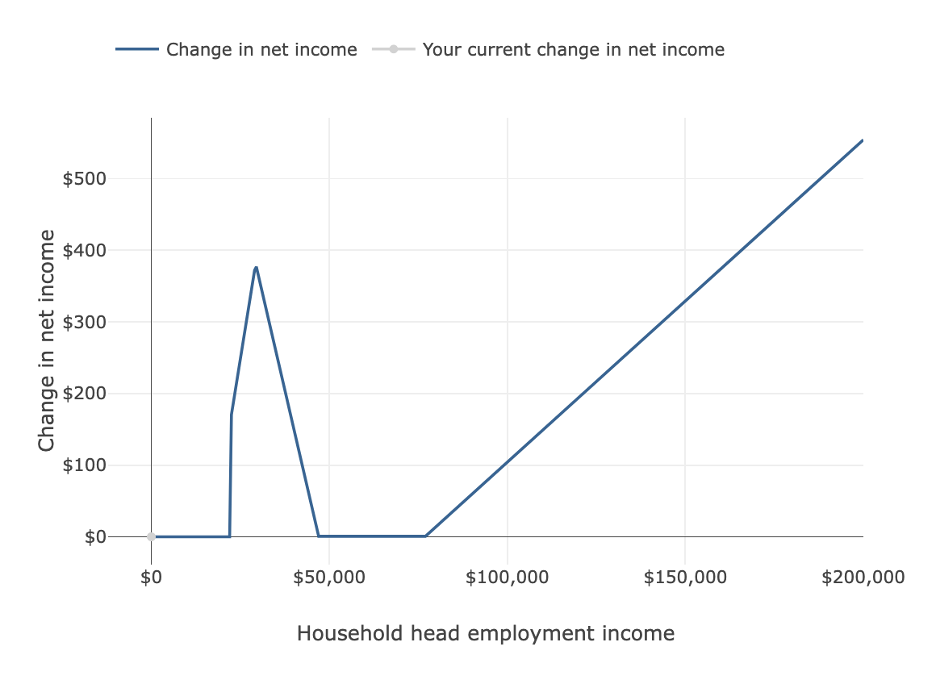

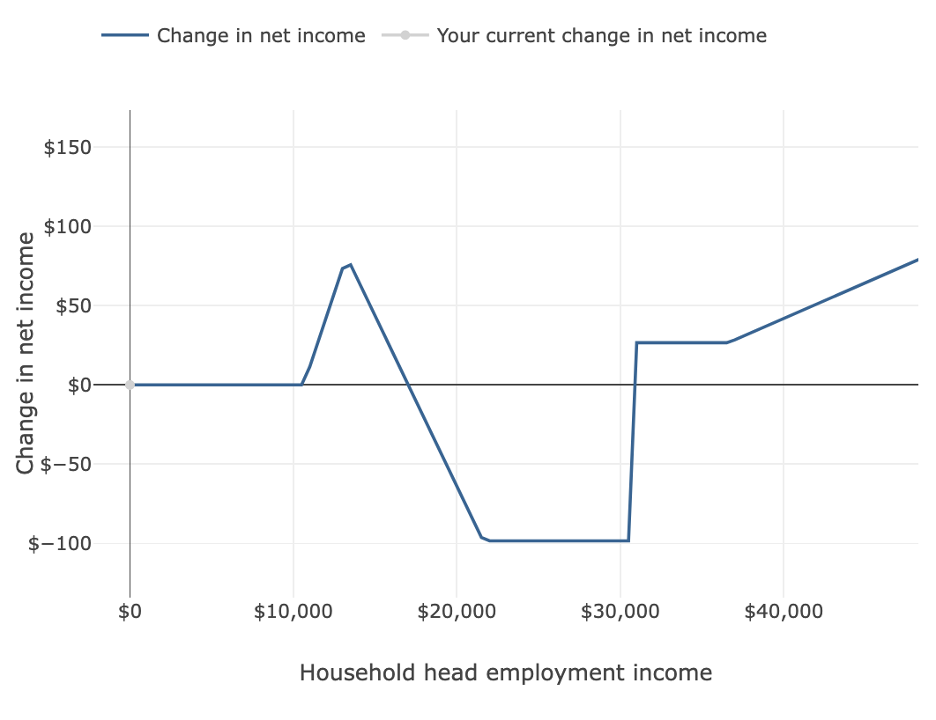

For an able-bodied single 55-year-old with no dependents, the bill would

We must reiterate that our model does not include eliminating the food sales tax, which may counteract some of these losses. A single individual with no dependents earning more than $17,676 annually is

With that in mind, the chart below shows our projected

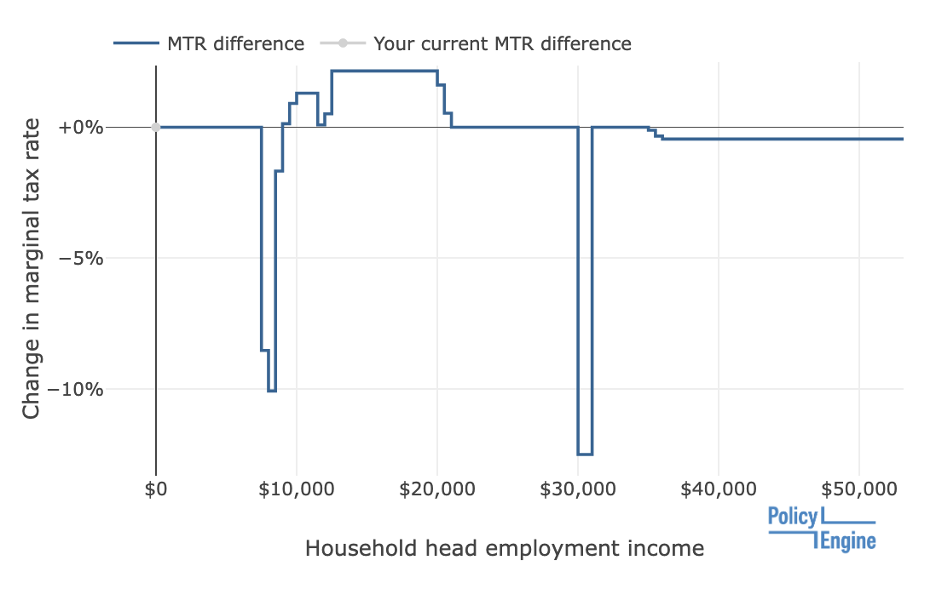

The sudden spike above $30,000 occurs when they are no longer eligible for the FSTC, so SB169 would lower their income tax rate without causing them to lose these benefits. Net income gains continue to increase linearly above $35,500 as the bill reduces the rate for individuals in the top marginal tax bracket from 5.7% to 5.25%.

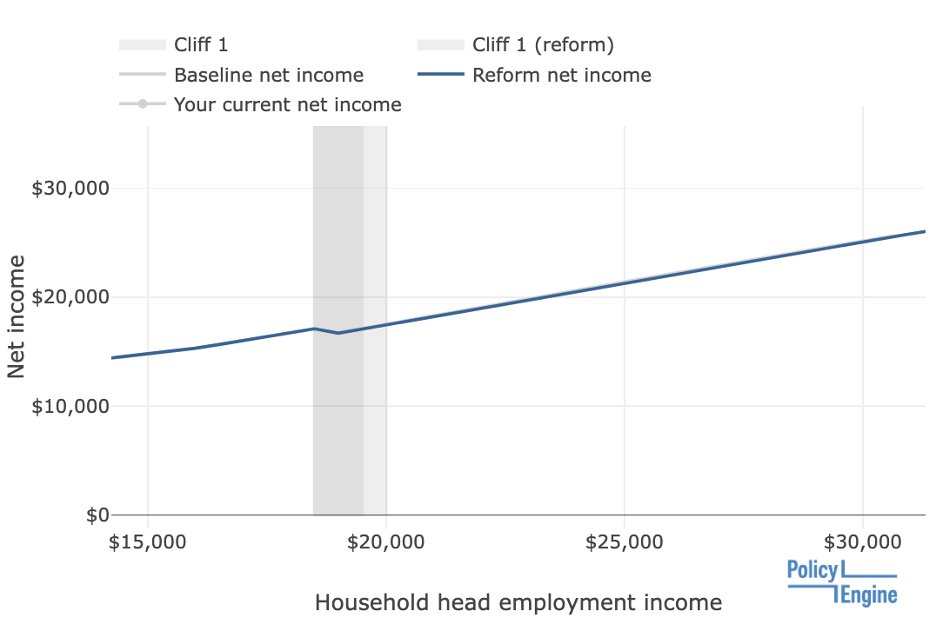

Currently, a 55-year-old with no dependents between $18,500-$19,500 of AGI faces an effective marginal tax rate greater than 100%, meaning their net income actually declines as their earnings increase. Under SB169, this cliff would extend to $20,000 of AGI, as shown by the chart below.

The following chart shows the

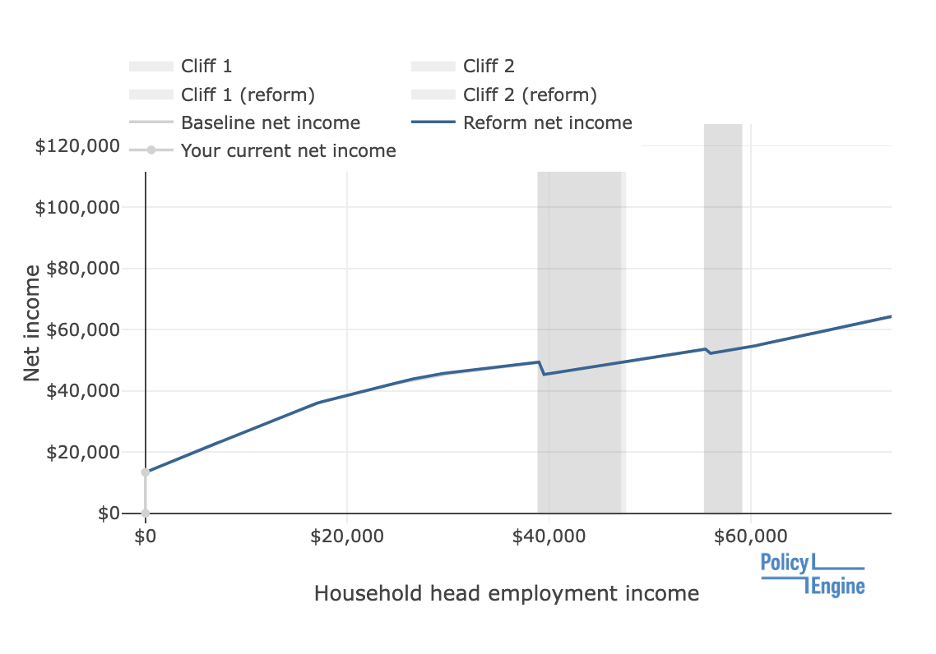

Next, we will consider the impacts of SB169 on a 40-year-old married individual with two children. As shown by the next chart, the bill would

However, SB169 would slightly extend a cliff between $39,00-$47,500 for families with these characteristics and leave a second cliff between $55,500-$59,000 intact. This results from the increased marginal tax rates it would create in that earnings range.

Next, we will consider the

How would SB169 affect Kansas as a whole?#

To simulate the state-wide impacts of SB169 in 2023, navigate to ‘compute the impact of policy reforms’ from PolicyEngine’s homepage, click on ‘find an existing policy,’ select ‘

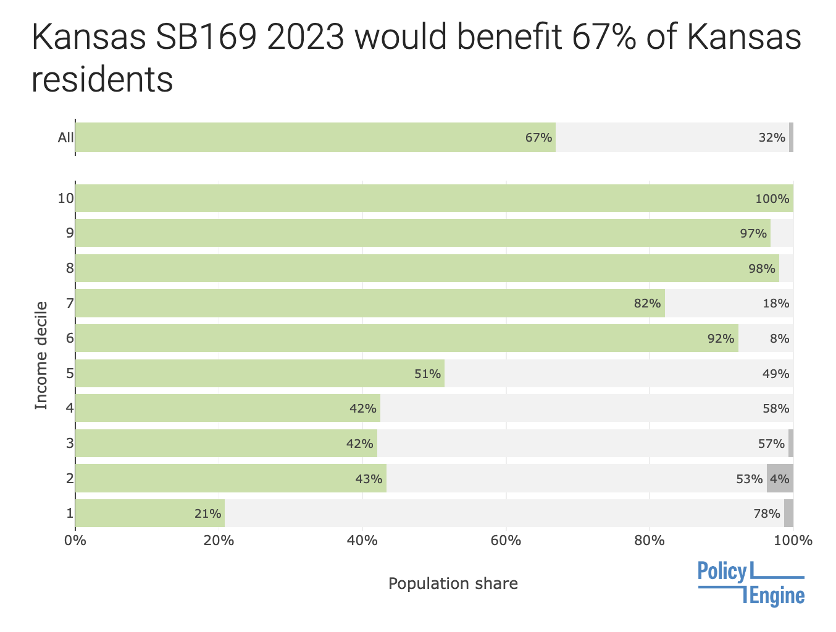

Those benefits would

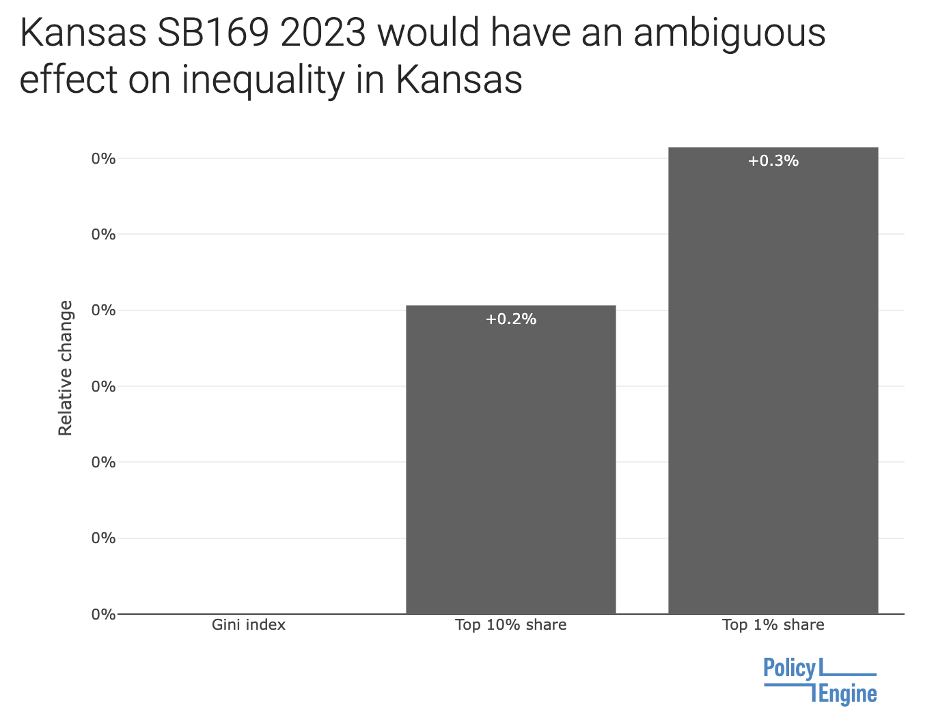

Despite causing gains in net income for many individuals, the bill would not affect

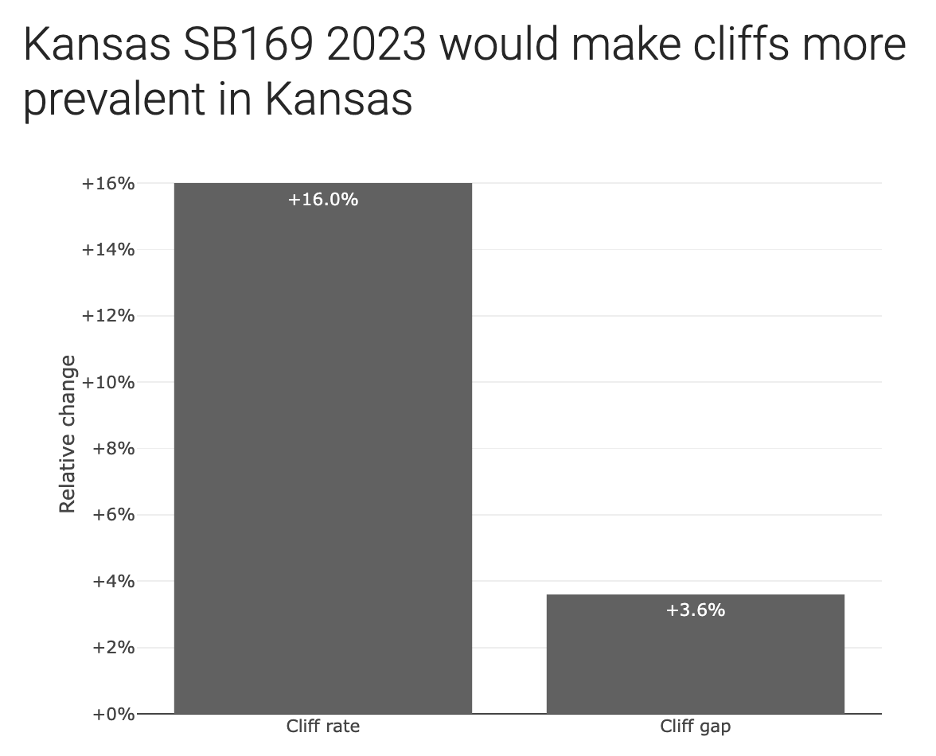

Lastly, the bill would make cliffs

As demonstrated when we considered specific individuals, the bill increases marginal tax rates in particular earning ranges in ways that interact with the phaseout of benefits like SNAP and the FSTC to cause these cliffs.

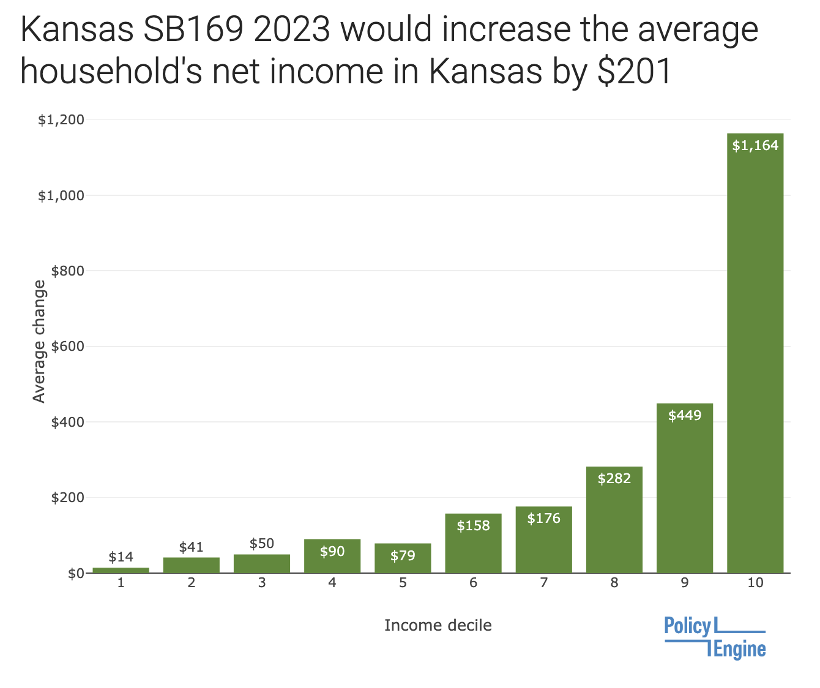

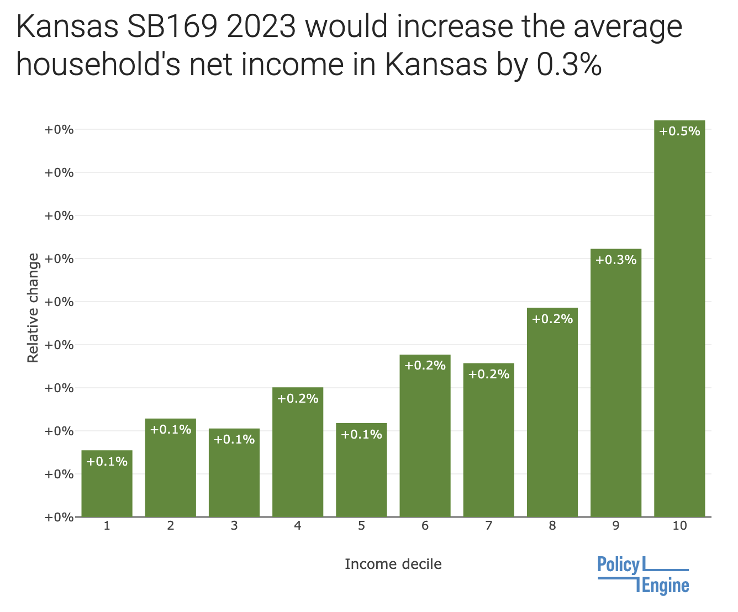

If enacted, SB169 would replace Kansas’s progressive tax system with a flat income tax rate of 5.25% and alter several other tax provisions. According to PolicyEngine’s model of a subset of income tax provisions, the reform would result in a revenue loss of around $240 million for the state while increasing the average household’s net income by $201, with people in higher income deciles gaining the most.

We forecast that 0.6% of Kansans would experience losses due to SB169 eliminating the Food Sales Tax Credit, primarily in the bottom three income deciles. However, our model does not account for eliminating the food sales tax, which may offset these losses for some individuals.

The bill would not impact Kansas’s poverty or deep poverty rates, and though the share of income earned by the wealthiest citizens would increase, the Gini index would remain unchanged. Lastly, the reform would make income cliffs more prevalent, with the cliff rate rising by 15.8% and the cliff gap increasing by 3.6%.

As policymakers and Kansans weigh the benefits and drawbacks of this reform, it is essential to consider these impacts and their broader implications for the state’s tax and benefits system.

arthur wright

Researcher at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.