The Proposed New York City Child Tax Credit

Analysis of Senate Bill S2238, introduced by Senator Andrew Gounardes.

Contents

Background

Household Impacts

Citywide Impacts

Conclusion

As New York’s legislative session progresses, lawmakers are proposing various changes to the state’s income tax code.

-

Generate $93.3 million in state revenue

-

Affect 57% of NYC residents, with 32% seeing increased net income and 25% seeing decreased net income

-

Lower poverty by 0.8% and child poverty by 2.0%

-

Reduce the Gini index of income inequality by 0.3%

Background#

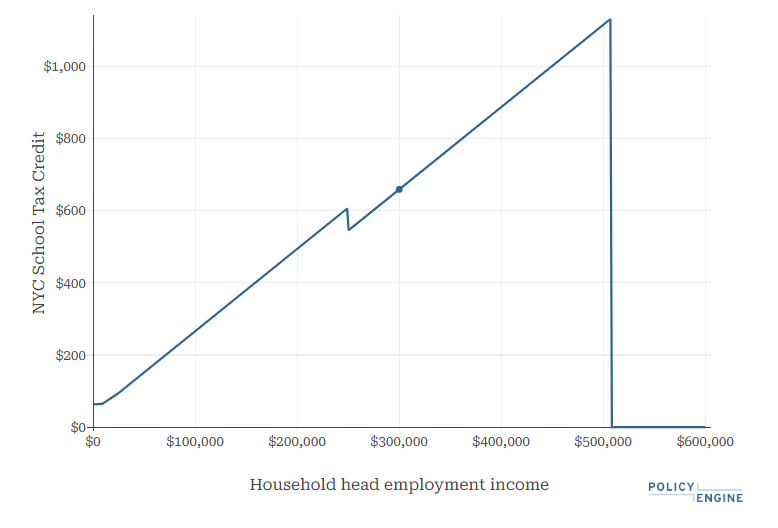

The School Tax Credit, like other tax credits available to New York City residents, is administered through the New York State tax system. While these credits specifically benefit residents of NYC, they are funded at the state level as part of New York State’s broader tax and revenue structure. New York City income tax revenue flows to the state’s tax administration before funds are allocated back to the city through various programs and credits. The current STC structure consists of two components that vary based on filing status and income level:

-

The fixed amount provides $63 ($125 for joint and surviving spouse filers) to filers with state AGI at $250,000 or less.

-

The rate reduction amount increases with taxable income and is limited to filers with taxable income below $500,000. For filers with taxable income below $12,000 ($21,600 for joint filers and $14,400 for heads of households), the rate reduction amount equals 0.171% of taxable income; above that threshold, it equals 0.228% of taxable income.

Figure 1 shows the total amount of the School Tax Credit for a single filer based on household income.

Figure 1: NYC School Tax Credit for a Single Filer Based on Household Income

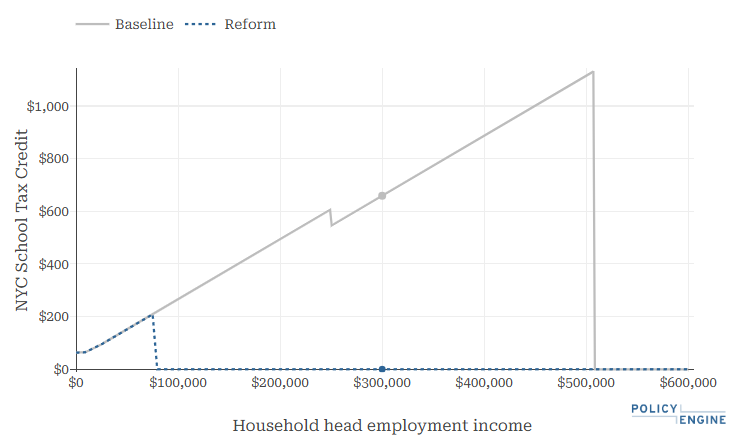

Senate Bill S2238 would reduce the School Tax Credit at $5 per $100 of earnings exceeding $75,000 ($150,000 for joint and surviving spouse filers). The proposed structure of the STC can be seen in Figure 2 below.

Figure 2: Reformed vs. Current School Tax Credit for a Single Filer Based on Household Income

At the same time, the legislation would introduce a $300 fully refundable Child Tax Credit for NYC residents with children under the age of 18. This credit would also phase out at 5%, starting at $75,000 and $150,000.

Household Impacts#

The impact of Senate Bill S2238 varies based on household composition and income level. To understand this, let’s examine different family examples and how the proposal changes their net income.

See how a New York City Child Tax Credit would affect your household with our

Table 1: Impact of Senate Bill S2238 on Various Household Compositions

A single adult with $50,000 in earnings and zero children would continue to receive their current School Tax Credit at $152

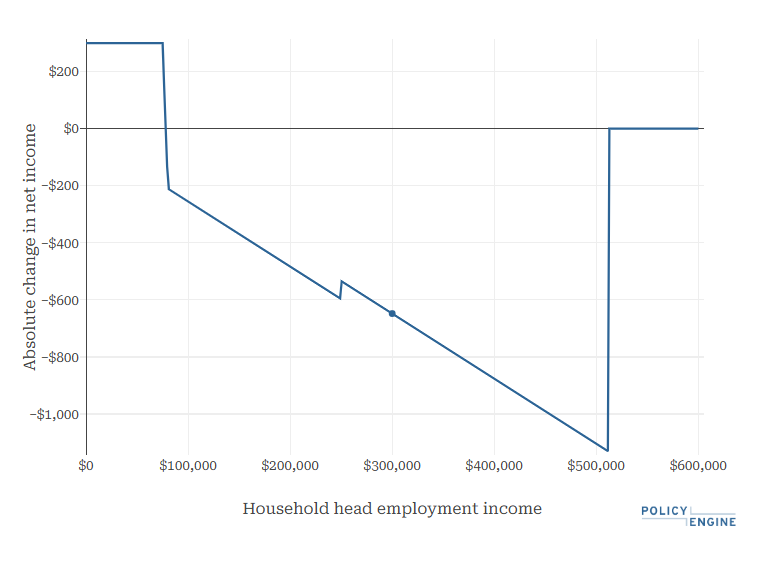

For a single parent of one making $50,000 a year, their net income would increase by $300 as their STC would also remain unchanged at $152, but they would now receive the $300 NYC CTC. The STC phases out from $75,000 to $78,040 of earnings, and the CTC phases out from $75,000 to $81,000, so at $85,000 of earnings, their net income falls by $221.

Figure 3: Change in Net Income for a Single Parent of One Child Under Senate Bill S2238 Based on Household Income

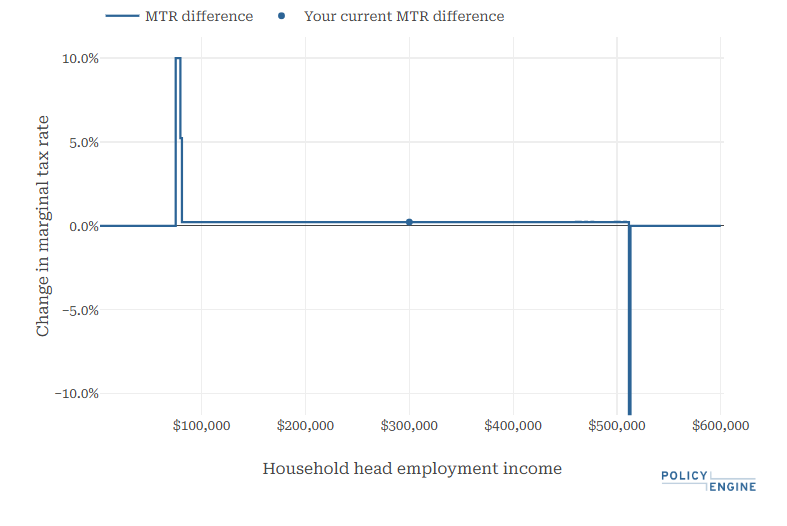

Figure 4: Change in Marginal Tax Rates for a Single Parent with One Child Based on Household Income

In summation, households with no children are unaffected if their earnings are less than $75,000 (or $150,000 if filing jointly). Households with children below these thresholds would receive an additional $300 for each child under 18. Above these thresholds, the credits gradually phase out, but families with children would remain better off until reaching their “breakeven point” — where the change in net income becomes zero before turning negative. Beyond the breakeven point, a family’s net income decreases until their taxable income reaches $500,000, at which point their change in net income returns to zero since they do not qualify for the current School Tax Credit or any proposed changes. Table 2 displays the breakeven points for single and married households with zero to four children.

Table 2: Breakeven Points by Household Composition

Rounded to the nearest $100.

Using PolicyEngine’s microsimulation capabilities through 3 years of pooled data (2021–2023) from the Current Population Survey (CPS), we can also estimate the impact of Senate Bill S2238 on New York City at large.

Citywide Impacts#

Phasing out the School Tax Credit would raise

As displayed in Figure 5, the proposed legislation provides net benefits to the

Furthermore, while the average dollar amount gained in each decile in the bottom half of the distribution would vary, households in these deciles would see their net income increase

Figure 5: Average Benefit of Senate Bill S2238 by Income Decile

Fourteen percent of residents in the

Figure 6: Winners and Losers of Senate Bill S2238

Senate Bill S2238 would lower the city’s Supplemental Poverty Measure

Figure 7: Poverty Impact of Senate Bill S2238

Finally, the city’s Gini index of income inequality would

Conclusion#

Senate Bill S2238 would limit the School Tax Credit by phasing out benefits at 5% beginning at $75,000 ($150,000 for joint and surviving spouse filers). The legislation would also establish a $300 NYC Child Tax Credit for children 17 and under, phasing out at the same parameters as the reformed STC. Childless households under the phaseout thresholds would be unaffected, while families with children below $75,000 ($150,000 for joint and surviving spouse filers) would gain $300 per eligible child. Senate Bill S2238 would raise $93.3 million in state revenues in 2025. 32% of NYC residents would see their net incomes increase, including 40% of those in the bottom half of the household income distribution. A quarter of the NYC population would see their tax liability increase. Finally, the city’s poverty level, as measured by the SPM, would decrease, including a 2.0% reduction in child poverty.

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

We invite you to explore our

-

The childless adult would receive the STC’s fixed amount of $63, plus the rate reduction portion. With $50,000 in annual earnings, their taxable income is $42,000 as they receive New York’s $8,000 standard deduction. 0.171% of the first $12,000 is $20.52. 0.228% of the remaining $30,000 is $68.40. Combined the rate reduction amount is around $89. $63 plus $89 is $152, the adult’s total STC.

↩ -

The School Tax Credit amounts for a childless adult and a single parent who earn $85,000 are not the same due to the differences of the phase in rate thresholds of the “rate reduction” portion of the STC. The childless adult is a single filer while the single parent can use the head of household filing status.

↩ -

Note that these income deciles are based on the national income distribution, rather than NYC income distribution.

↩ -

PolicyEngine’s analysis shows that Senate Bill S2238 would increase the share of total net income held by the top 1% of households by less than 0.1%. This may be a relative effect rather than an absolute benefit to the top 1%. Since households in the top 1% typically have taxable incomes above $500,000, they would be largely unaffected by the bill’s provisions. However, the bill would reduce total net income held by all New Yorkers (by raising $93.3 million net tax revenue), leaving the top 1%’s constant dollar value a larger share of the total.

↩

david trimmer

Policy Research Fellow at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.