Oregon's nonrefundable exemption credit: a closer look

PolicyEngine computes the program's impact on Oregon and individual households.

Contents

The Household Impact

Step-by-Step Instructions for Estimating Impacts of Oregon’s Exemption Credit

Oregon’s nonrefundable exemption credit was created in 1983 to replace the personal exemption deduction. Since 1987, the state has indexed the credit to inflation. As a nonrefundable credit, its value is capped at one’s tax liability. Single and married filing separately statuses can claim the credit if their income does not exceed $100,000. For other statuses, the income cap is $200,000. In the 2022 tax year, eligible filers could claim a $219 credit for themselves, their spouse, and any dependents in the household. They can also claim additional exemptions if the filer or their spouse is severely disabled, or if they have a disabled child.

Using PolicyEngine, we can compute the exemption credit’s impact on the state of Oregon and individual households.

The Household Impact#

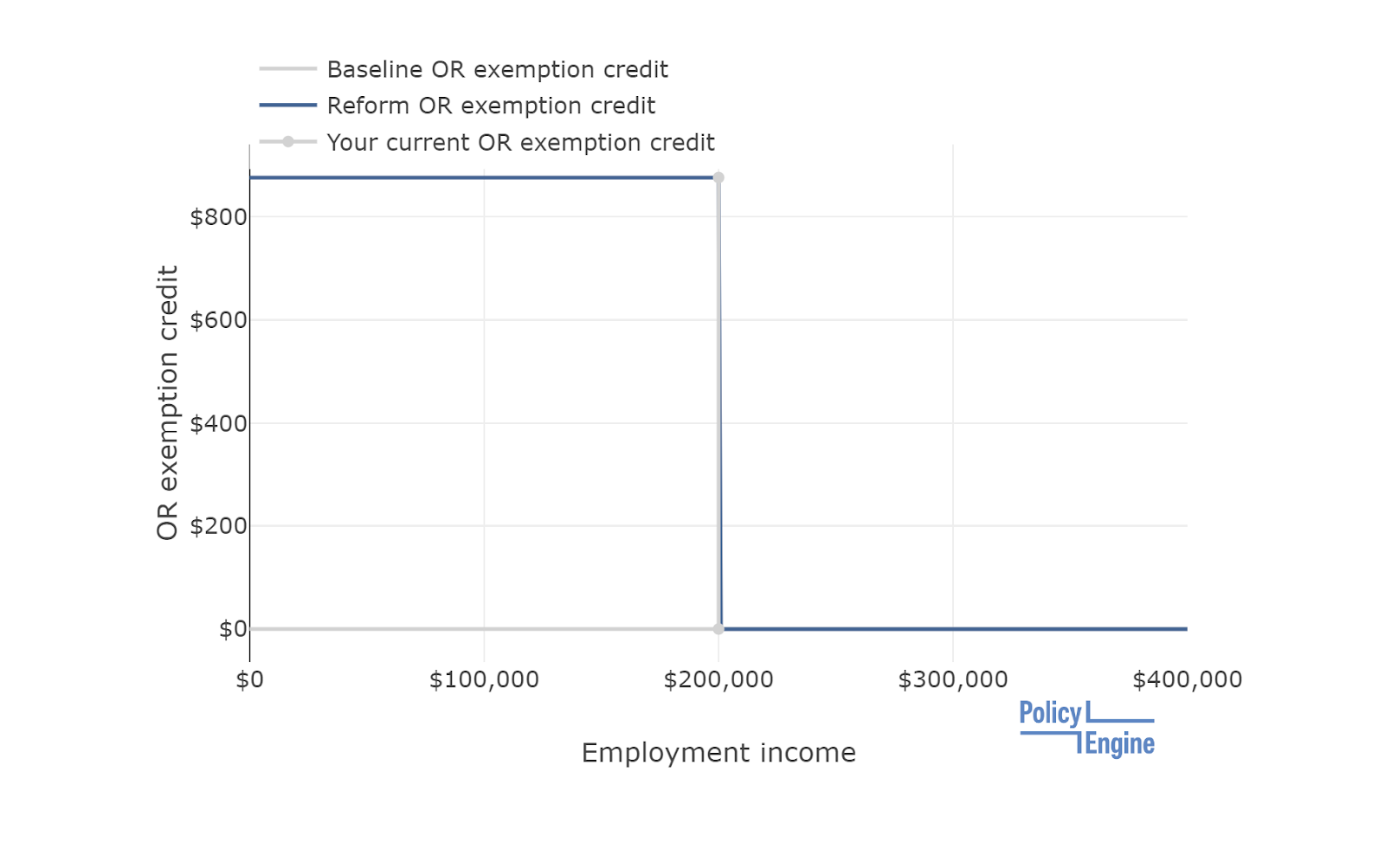

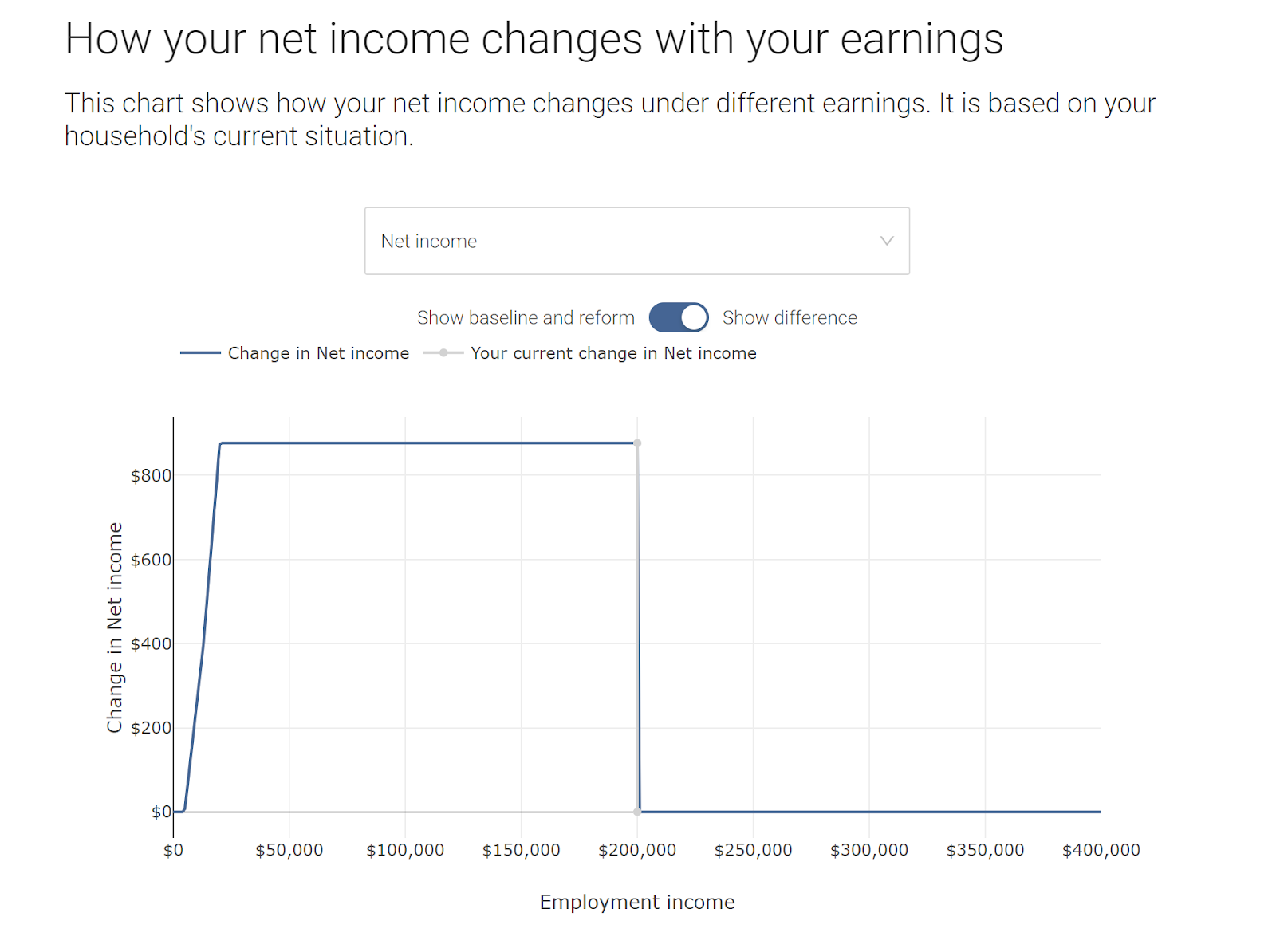

The exemption credit for a family of four (married with two children) is shown above. Making under $200,000 provides a credit of $876 ($219 * 4). To see how to define a household, check out our

Due to the credit’s non-refundability, the value phases in. The household would have to earn $21,000 to see the full value of the credit.

Step-by-Step Instructions for Estimating Impacts of Oregon’s Exemption Credit#

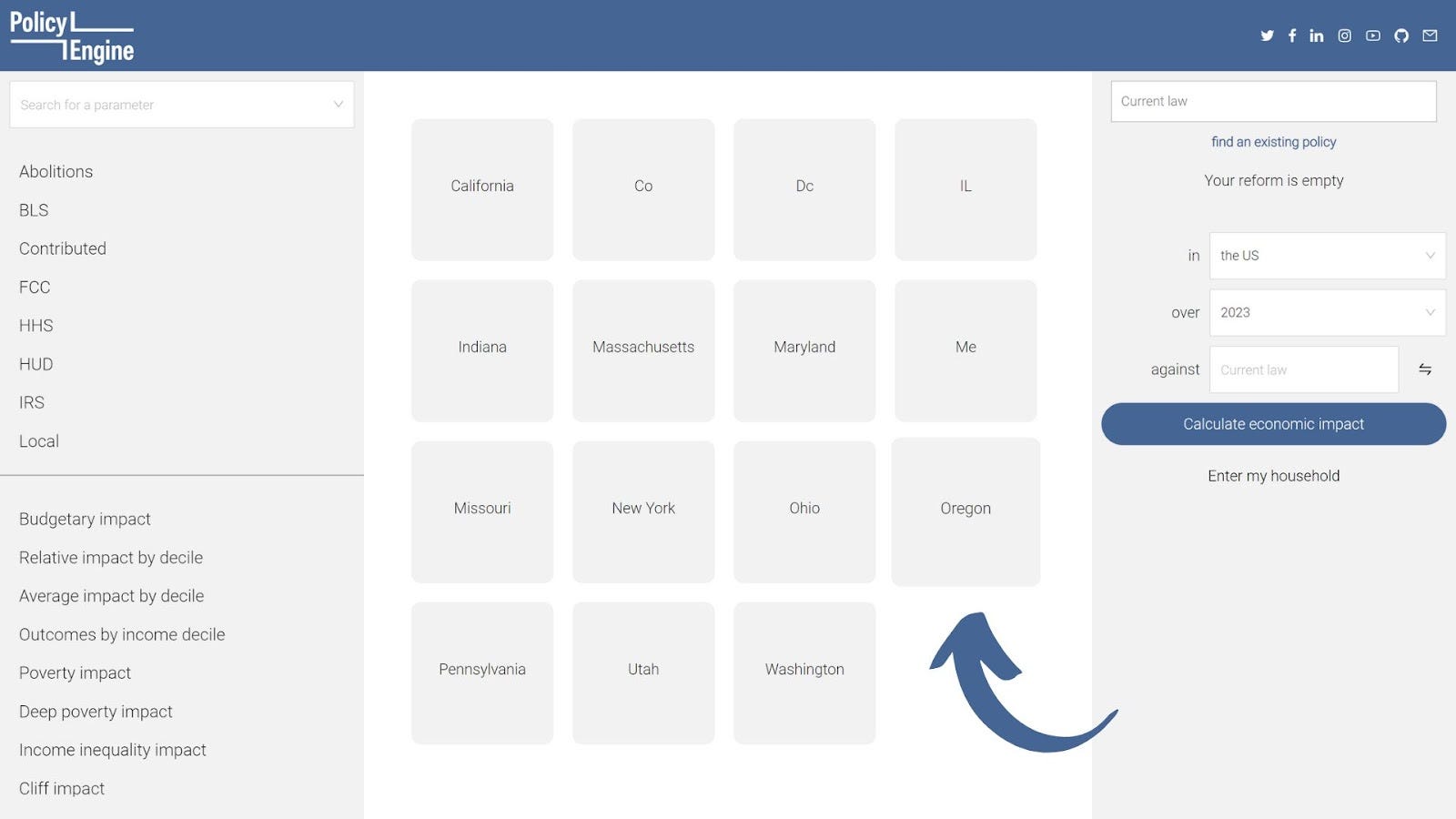

Select “compute the impact of policy reforms,” then “States.”

Enter “Oregon” for your state, then click through “taxes,” “income,” and “credits.”

Then, select “Exemption,” followed by “Oregon exemption amount.”

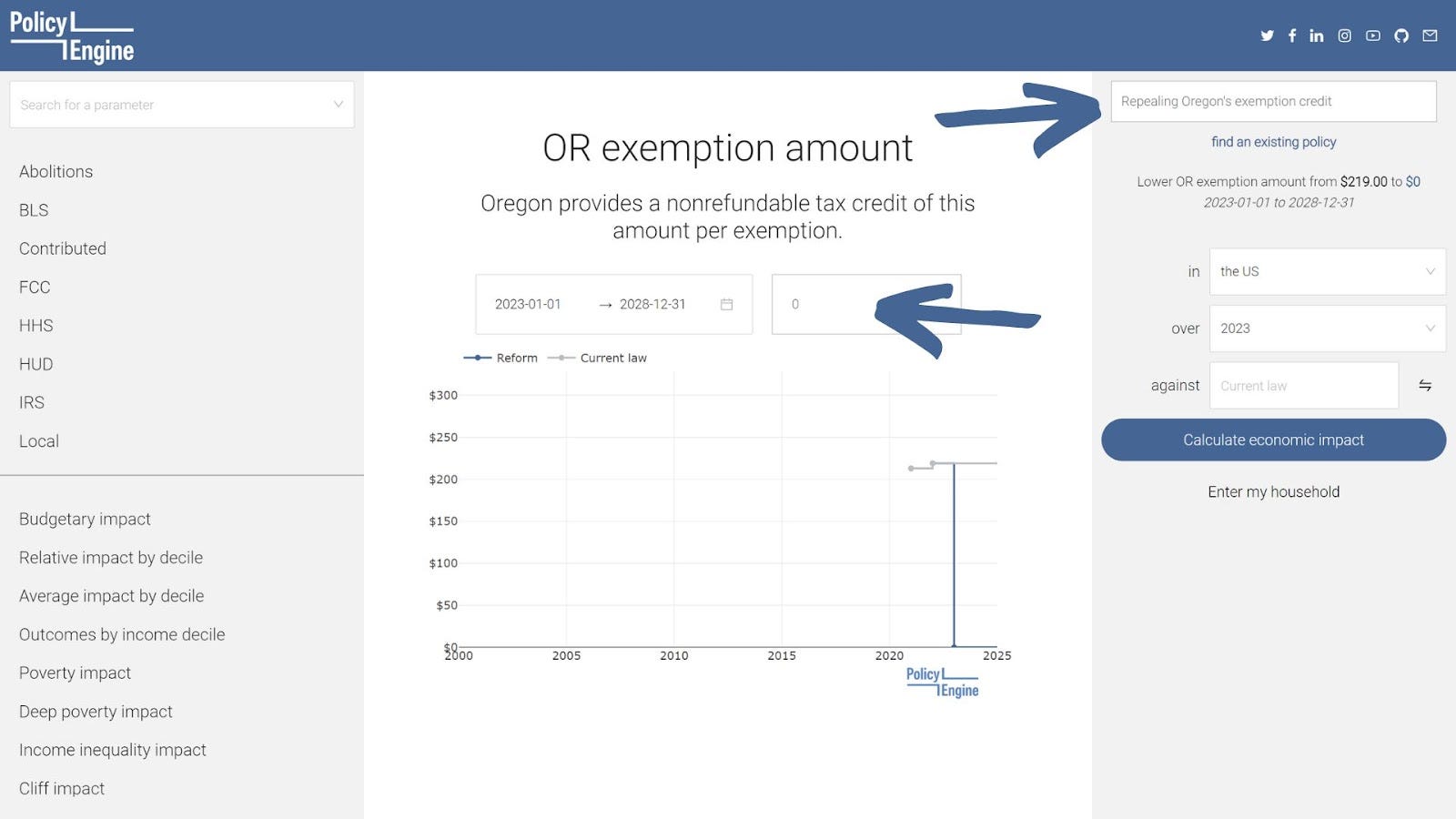

Enter 0 for the amount. You can also name your policy in the top right (“Repealing Oregon’s exemption credit” in this example).

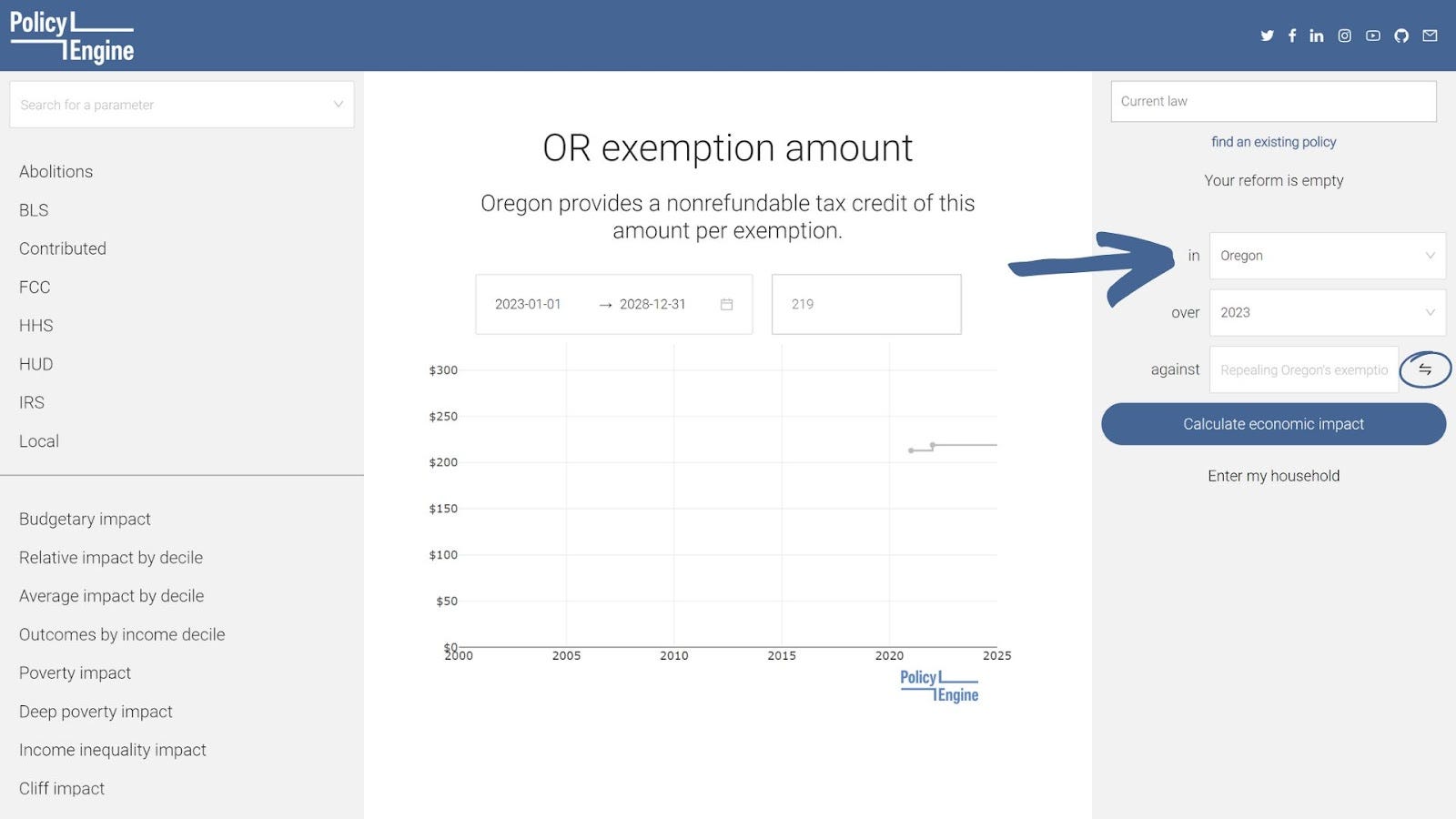

Then, press the arrows next to the “against” tab, followed by setting the reform to “in Oregon.”

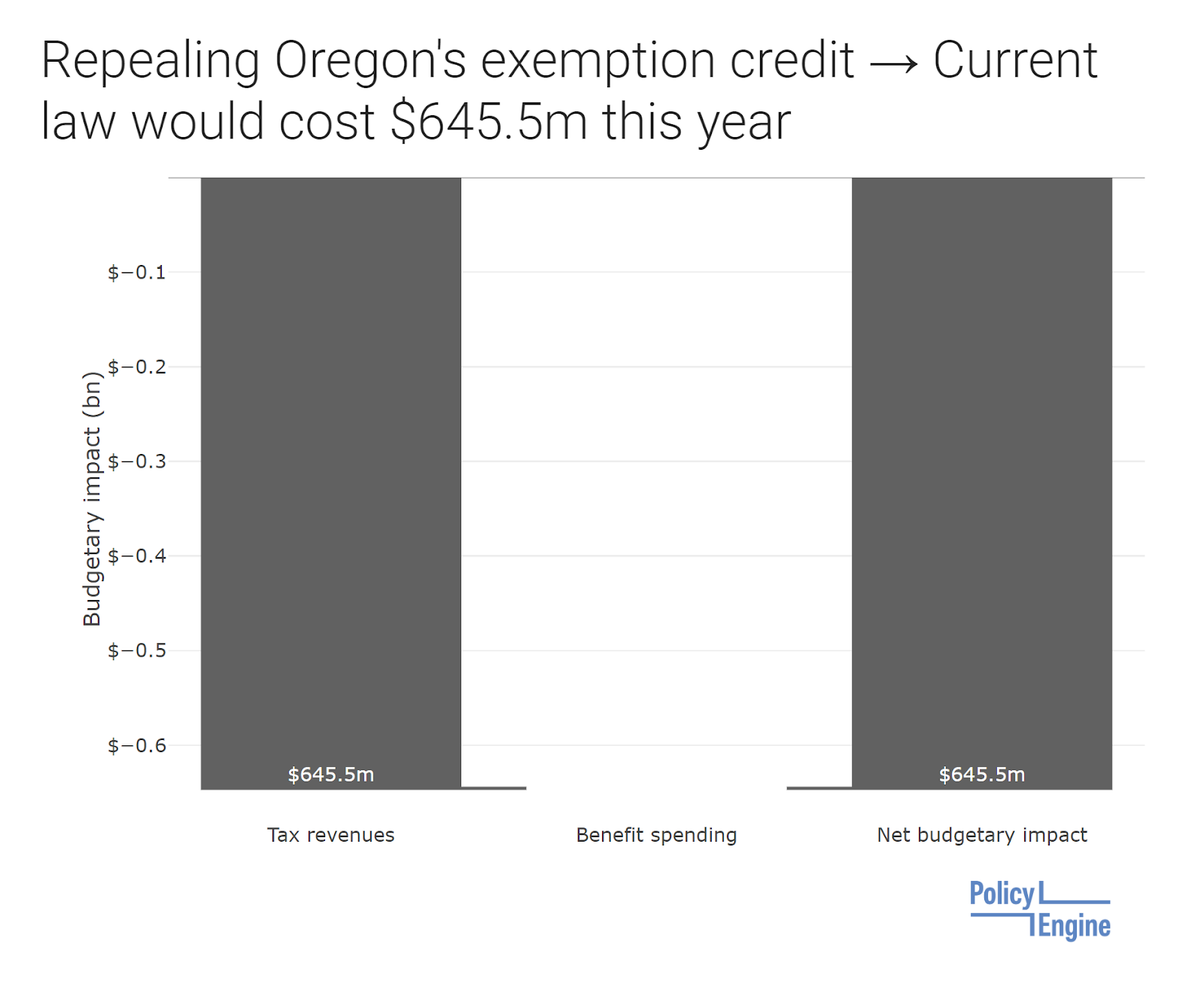

Select “Calculate economic impact” and choose which metric you would like to view (budgetary impact below)

We estimate that Oregon’s exemption credit

To compute other elements of Oregon’s income tax, visit

-

In the 2021–2023 period,

Oregon’s biennial tax expenditure report shows a revenue impact of $4.6 million for the child with disability credit (p.144), $4.5 million for the severe disability credit (p.149), and $1,308,900,000 for the personal exemption credit (p.200). $1.318 billion divided by 2 (tax years 2021 and 2022) is $659 million.↩

kevin foster

Researcher at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.