Restoring the American Rescue Plan's Earned Income Tax Credit Expansion

We review how the expansion works and model its impact with PolicyEngine US.

Contents

What is the Earned Income Tax Credit?

What are the current impacts of the childless EITC?

How did the ARPA expand the childless EITC?

Limitations of PolicyEngine’s EITC model

How would restoring the ARPA childless EITC expansion affect the US?

Earlier this month, the Biden Administration

The president’s announcement refers to the expansion of the Earned Income Tax Credit (EITC) temporarily enacted by the American Rescue Plan Act (ARPA) in 2021, which has since expired. This report describes ARPA’s EITC expansion for childless workers and PolicyEngine’s projected impacts of restoring it today.

What is the Earned Income Tax Credit?#

The EITC is a federal tax credit for low- and moderate-income working individuals and families,

A critical feature of the EITC is that it is a “refundable” credit — meaning that if the value of the credit exceeds taxes owed, the taxpayer receives the excess as a refund. It also phases in and out gradually. The credit amount increases as earned income increases, reaches a maximum, and then decreases as earned income exceeds the phase-out threshold.

Historically, the EITC did not support childless workers. That changed with the Omnibus Budget Reconciliation Act of 1993, which created a new credit formula that included low-income workers without qualifying children. In 2021, the American Rescue Plan

What are the current impacts of the childless EITC?#

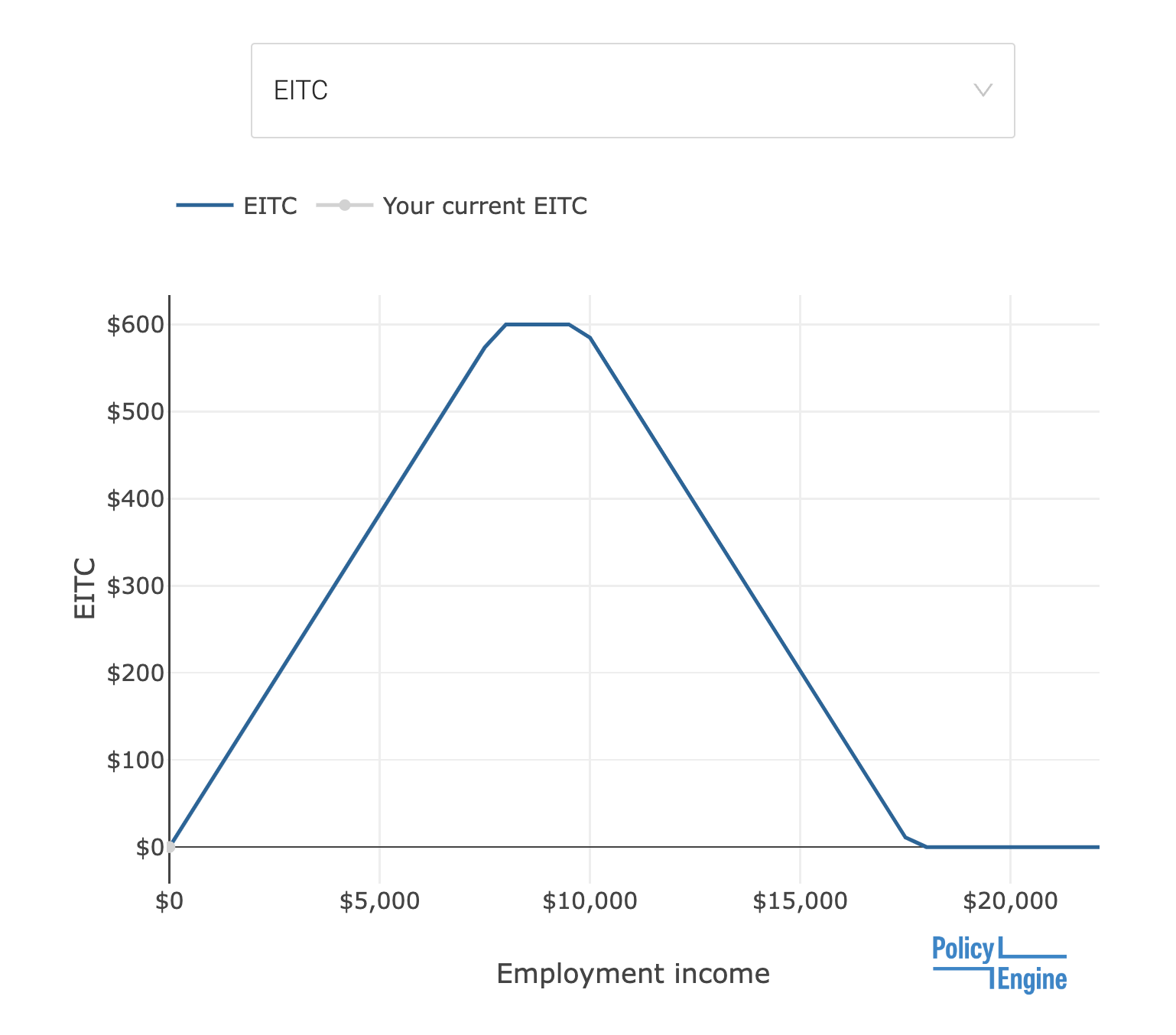

For each individual, the IRS

Correspondingly, such an individual faces a spike in their marginal tax rate between $17,500 and $19,000 of employment income when the EITC completely phases out. To model the impact of the childless EITC on marginal tax rates in PolicyEngine, visit

To compute the macro impact of the childless EITC using PolicyEngine,

Additionally, we project that the childless EITC

How did the ARPA expand the childless EITC?#

In 2021, ARPA made the following changes to the EITC for childless workers:

-

Lowered the applicable minimum age from 25 to 19

-

Eliminated the maximum age (previously 65)

-

Raised the maximum credit amount from $560

1 to $1,502 -

Raised the phase-in and phase-out rates from 7.65% to 15.3%

-

Raised the income threshold at which the phase-out begins from $5,280

2 to $11,610 -

Allowed separate filers in the same household to be eligible for the EITC

Limitations of PolicyEngine’s EITC model#

Before assessing PolicyEngine’s projected impacts of restoring these changes, it is necessary to note the limitations and assumptions of our model.

First, we do not model the full complexity of the modified minimum age, which contained exceptions for students, homeless youth, and former foster youth.

Second, our values for the maximum credit amount and income phase-out threshold are taken directly from ARPA itself, which did not contain inflation adjustments (as the provisions expired in the same fiscal year). Restoration of the ARPA EITC expansion would plausibly adjust these values for inflation; accordingly, our model’s projections may understate the impacts of reinstating these changes today.

As discussed above, we follow the CPS data’s understatement of low-income tax credits like the EITC.

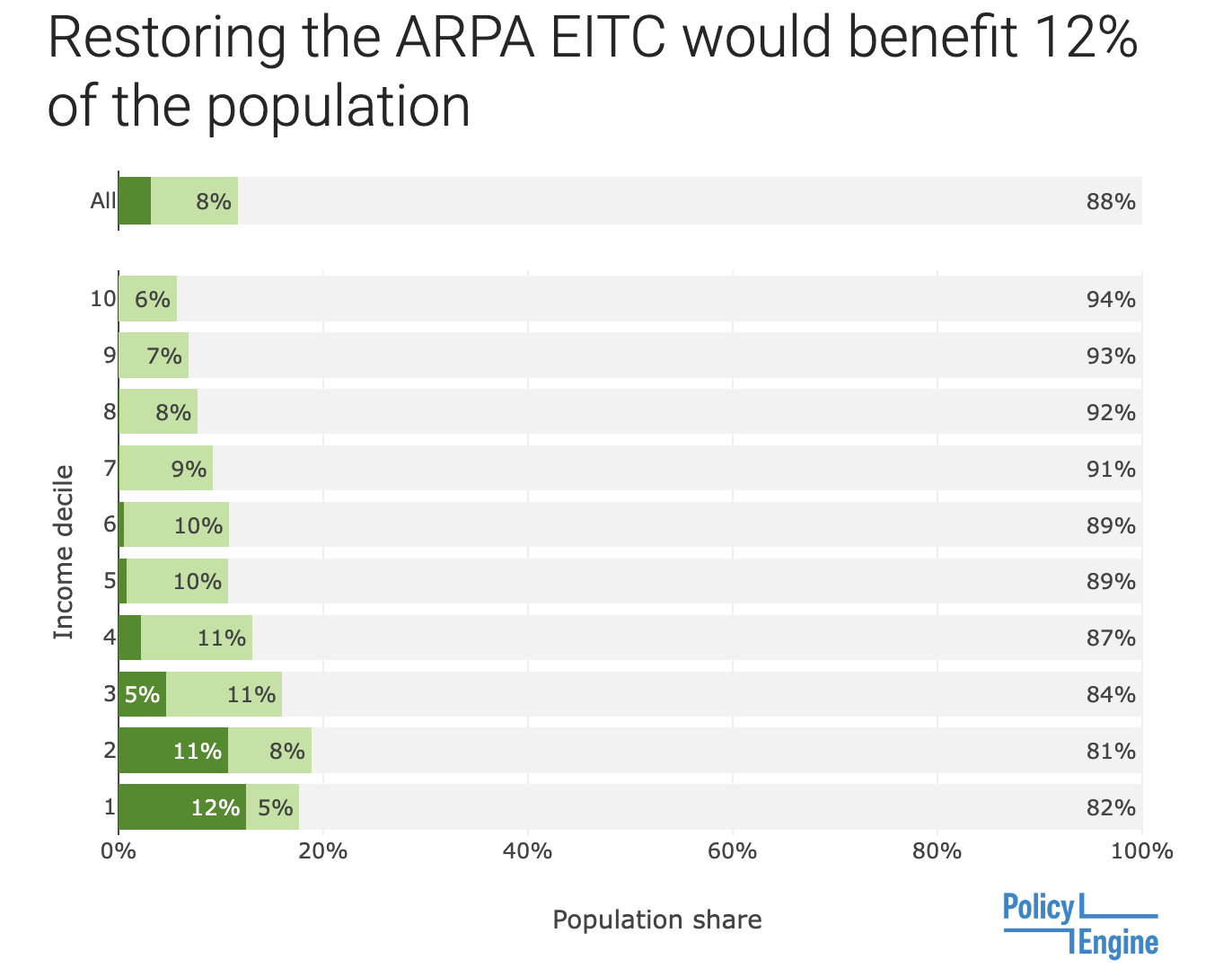

How would restoring the ARPA childless EITC expansion affect the US?#

To compute the population-level impacts of restoring ARPA’s EITC expansion, click on ‘find an existing policy’ and select ‘

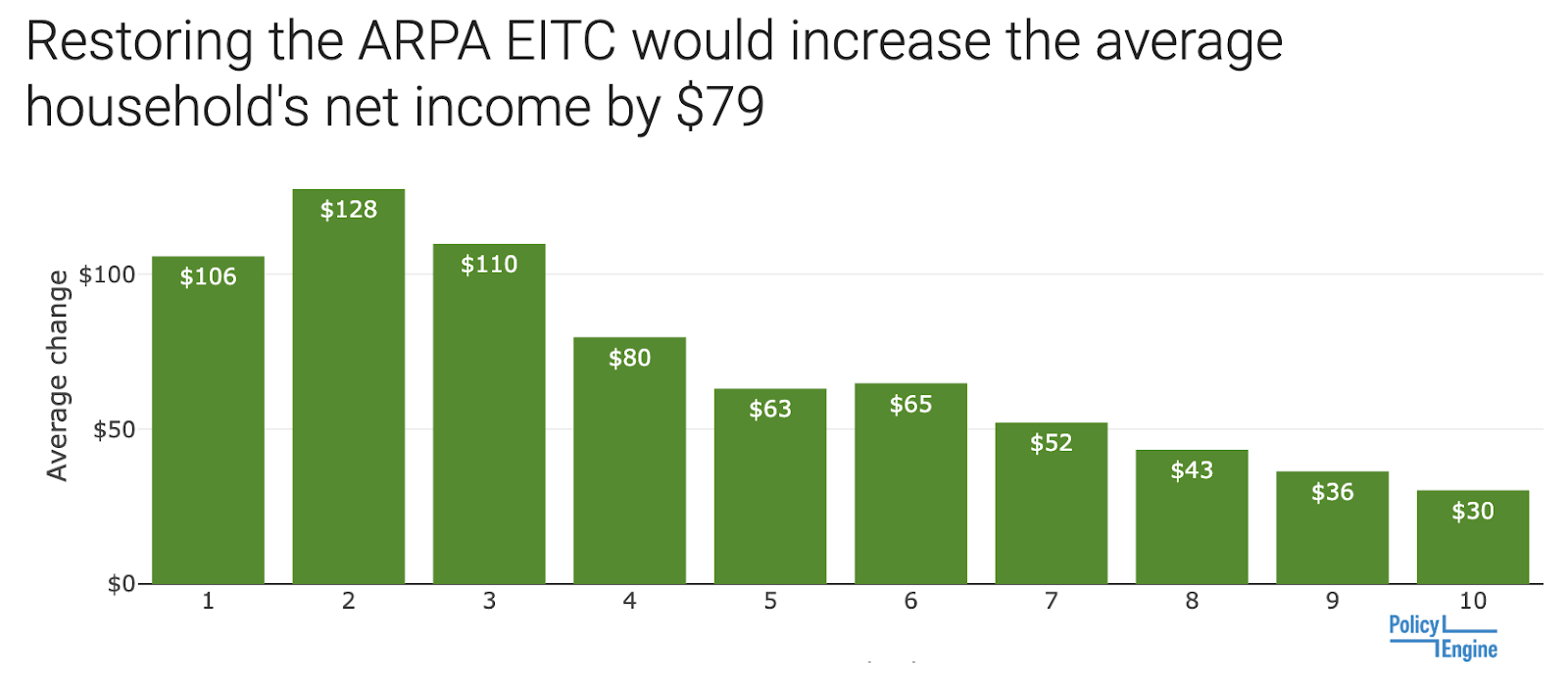

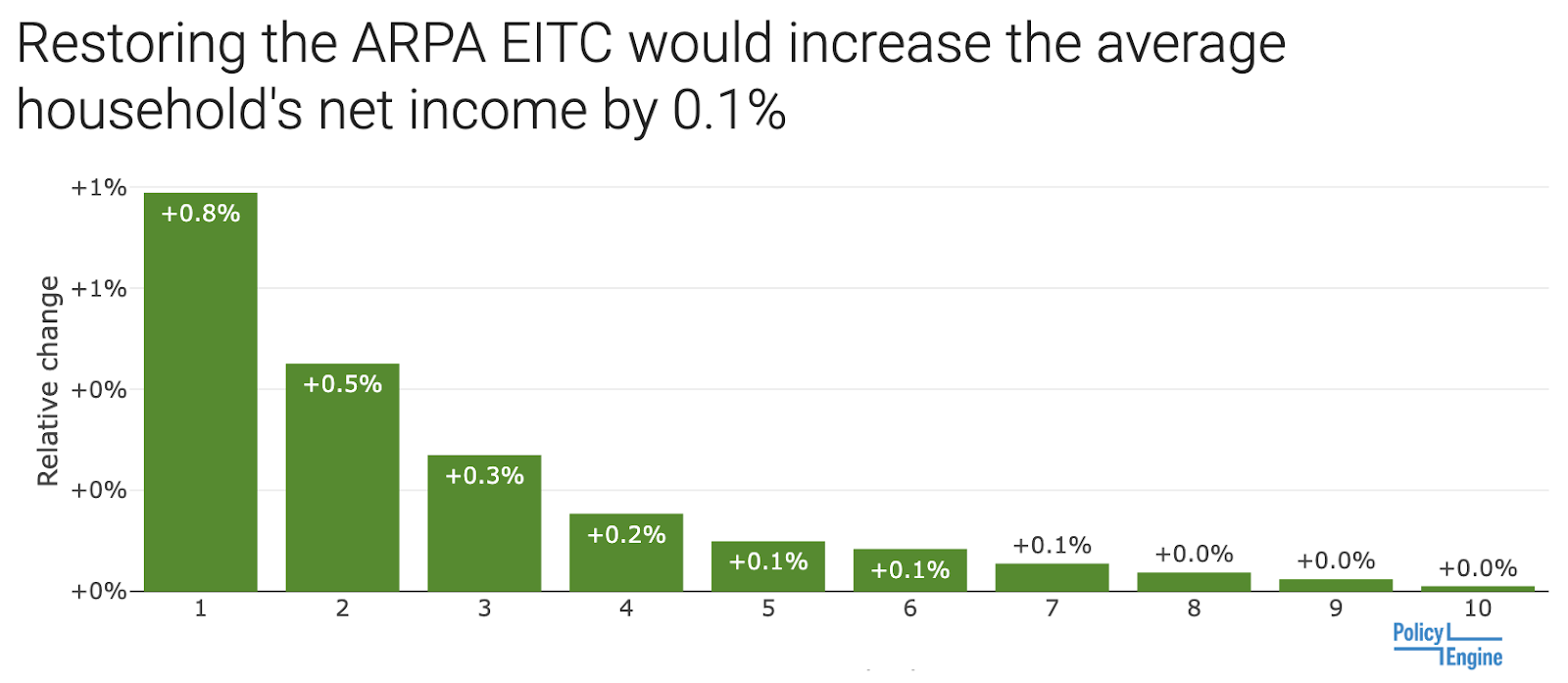

However, in percentage terms, the policy would provide

These benefits would

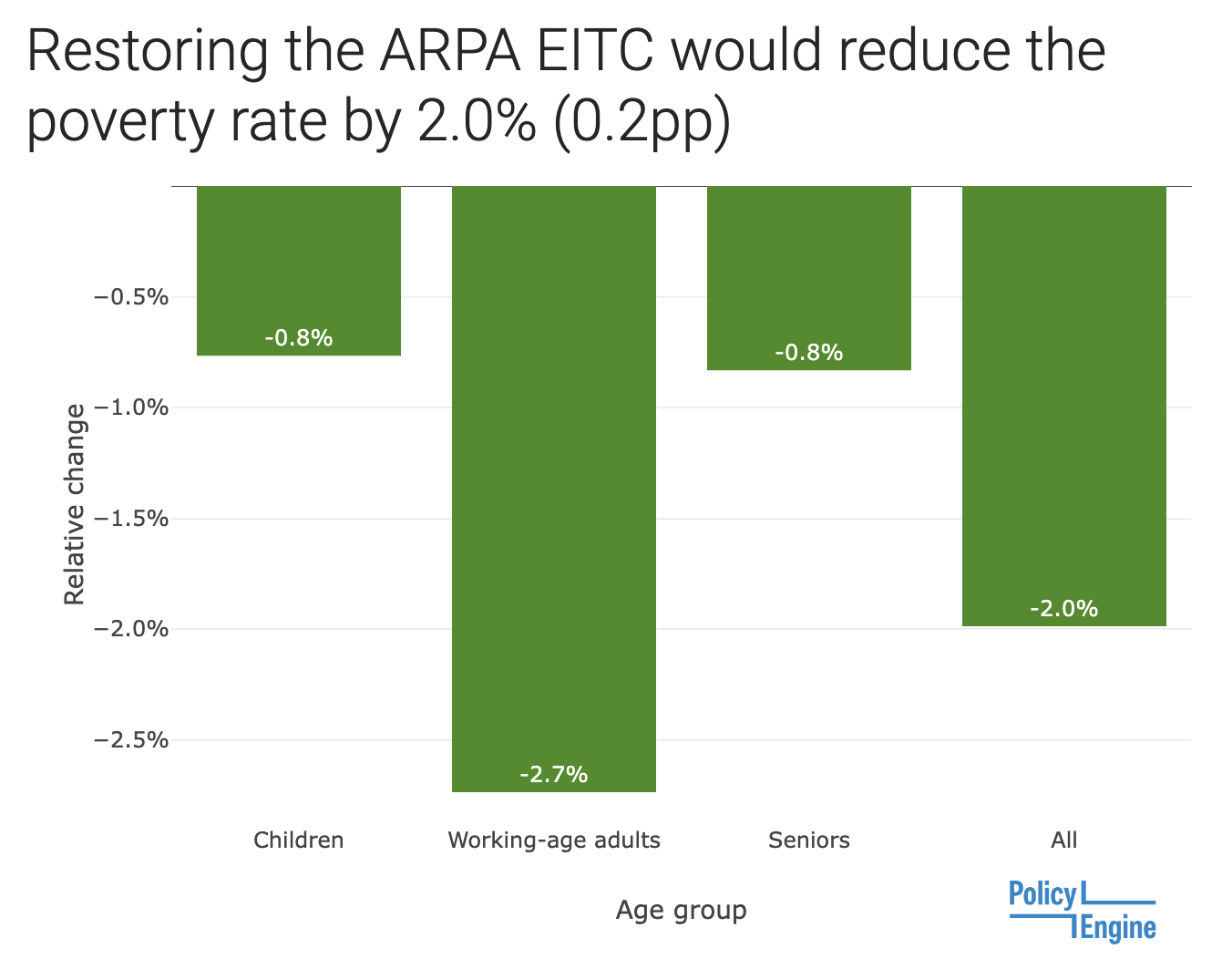

Our model of the Supplemental Poverty Measure indicates that the reform

Unsurprisingly, the most significant poverty reduction would be for working-age adults, as the expanded credits would accrue directly to employed adults without children. However, the child poverty rate would decline as well. This is likely due to adults living in households with children — but who are not themselves parents — newly qualifying for the EITC under the ARPA expansion. Additionally, the poverty rate for seniors would decline by 0.8%, likely due to ARPA eliminating the maximum age requirement.

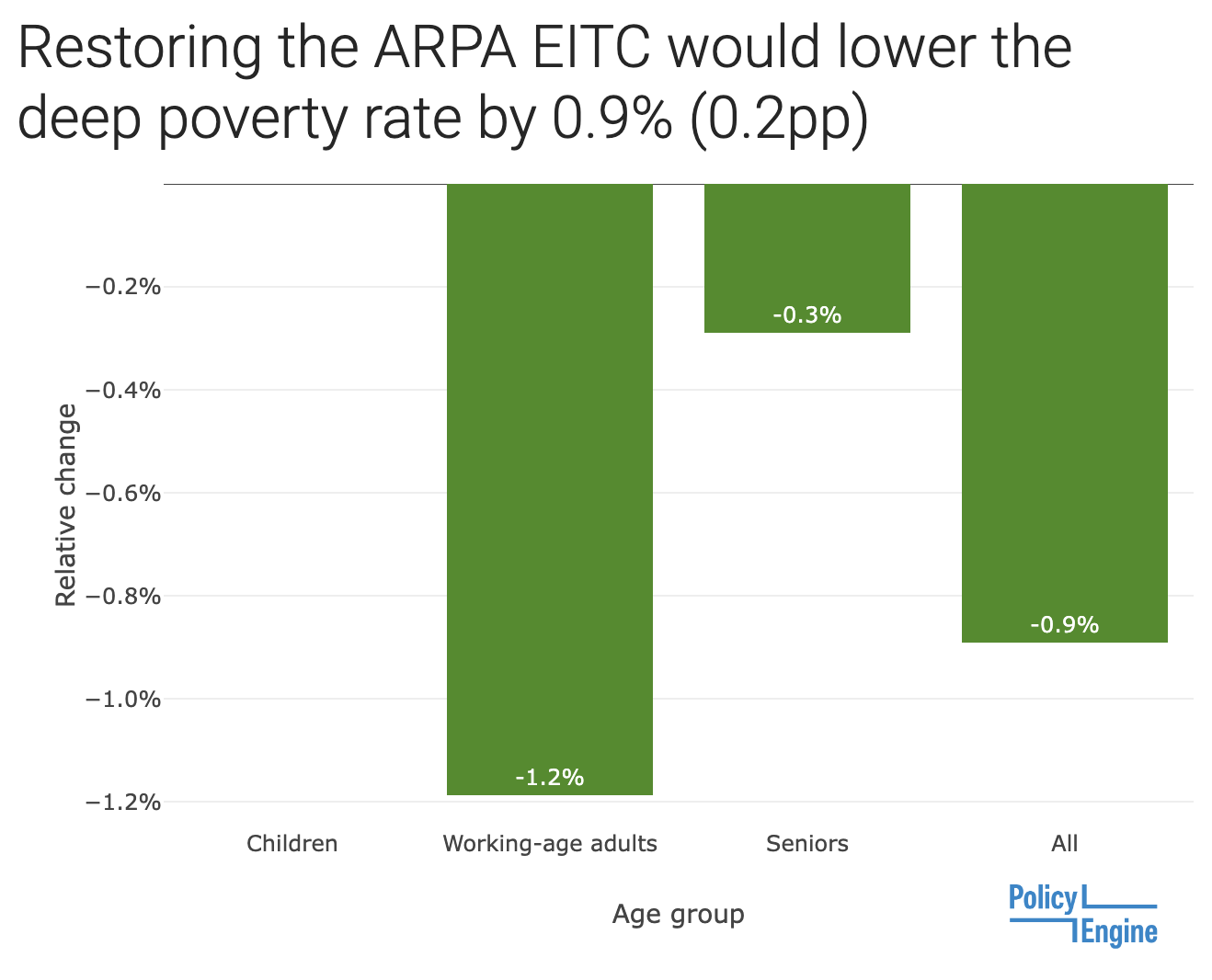

The expansion would also

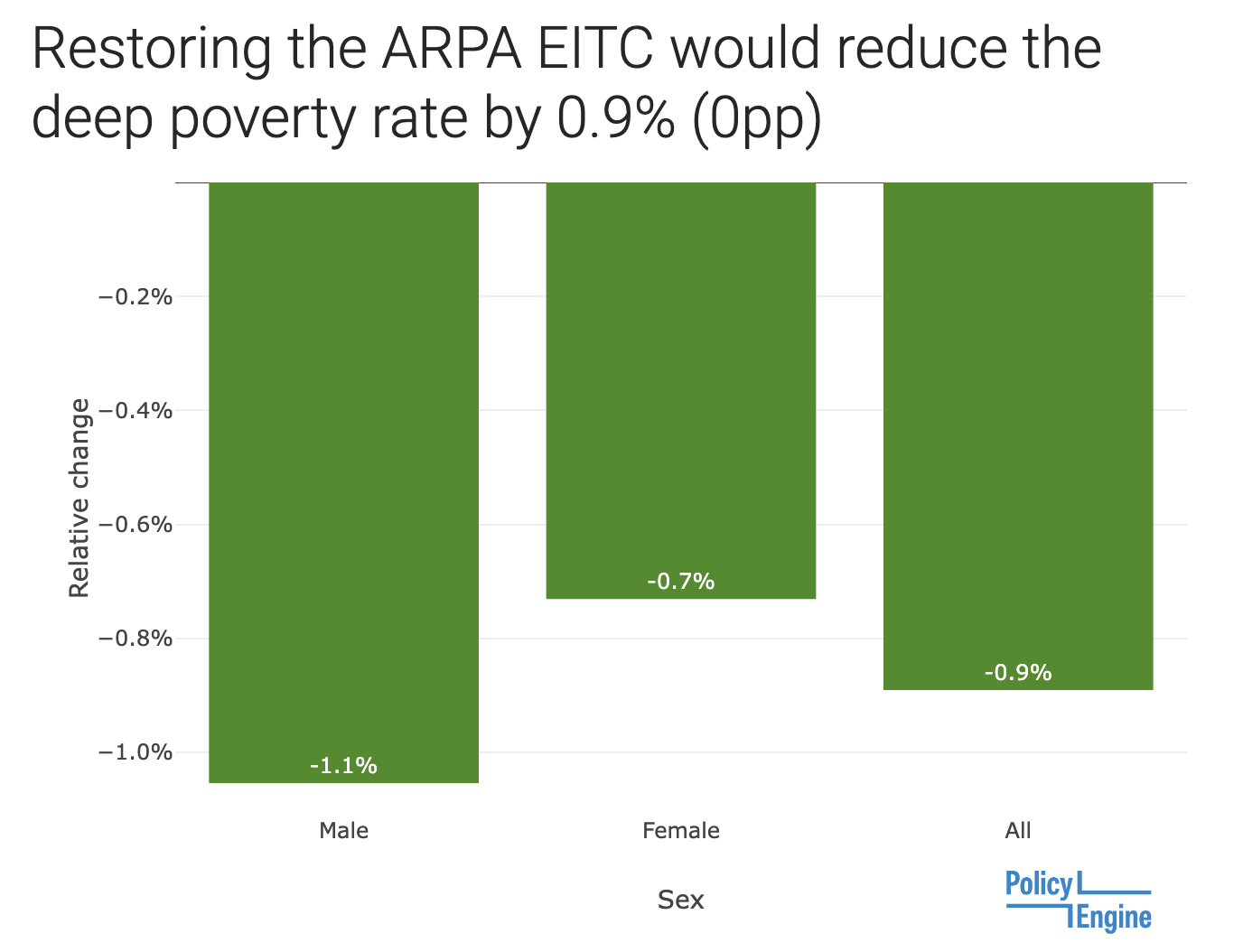

The reductions in

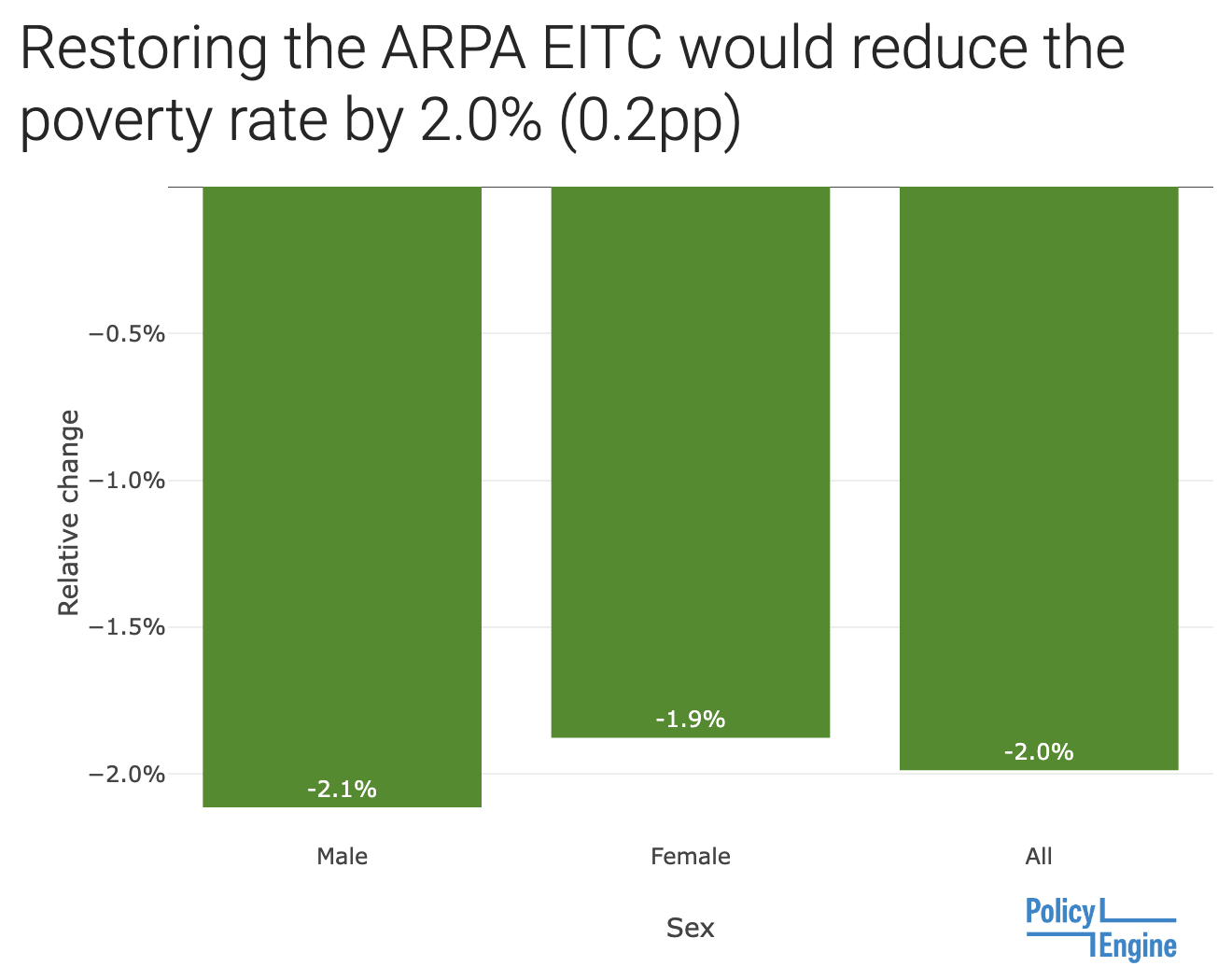

For men and women, the reform cuts deep poverty by about half as much as it cuts poverty.

Additionally, the reform would

Lastly, restoring the ARPA EITC would make “cliffs” (a.k.a.

The Biden administration has proposed making ARPA’s EITC expansion for childless workers permanent to “help pull low-paid workers out of poverty.”

We predict that restoring the ARPA expansion in 2023 would reduce the poverty rate by 2.0% and the deep poverty rate by 0.9% while increasing the average net income of households in the lowest three deciles by over $100.

While there are limitations to PolicyEngine’s EITC model, it provides a valuable tool for assessing the potential impacts of this policy change. The expansion would benefit lower-income workers and would, in fact, pull some of them out of poverty.

-

The value of $600 mentioned in the previous section is the inflation-adjusted figure for 2023.

↩ -

Today’s inflation-adjusted value is $9,800.

↩ -

The minimum age for “

specified students ” was only lowered to 24, and the minimum age for both “qualified former foster youth ” and “qualified homeless youth ” was lowered further to 18.↩

arthur wright

Researcher at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.