Preliminary analysis of the Wyden-Smith Child Tax Credit expansion

PolicyEngine estimates the impact of the reported compromise to expand the Child Tax Credit's refundable component.

Contents

How Wyden-Smith Would Reform the Child Tax Credit

Impact on a Household

Societal Impact

Conclusion

Politico’s Benjamin Guggenheim

From 2023 to 2025 — in our static model assuming full take-up — we project these provisions would:

-

Cost $16.4 billion, owing mostly to the more rapid phase-in rate

-

Lower poverty by about 1% and child poverty by about 4%

-

Benefit 6% of the population

-

Lower the Gini index of income inequality by 0.2%

How Wyden-Smith Would Reform the Child Tax Credit#

The Child Tax Credit (CTC) in the United States consists of two parts: the nonrefundable Child Tax Credit and the refundable Additional Child Tax Credit (ACTC). The Tax Cuts and Jobs Act of 2017 (TCJA) established the ACTC at $1,400 and the core CTC at $2,000 per child. The ACTC is indexed to inflation, which led to its increase to $1,600 by 2023 and $1,700 in 2024. The refundable portion of the CTC (ACTC) is available to families with earnings, phasing in at a rate of 15% of earnings above a certain threshold.

Guggenheim reported that the Wyden-Smith reform includes three parts:

-

Raising the refundable CTC amount: The maximum ACTC would rise from $1,600 to $1,800 in 2023, from $1,700 to $1,900 in 2024, and from $1,700 to the full $2,000 in 2025, with the amount indexed to inflation thereafter.

-

Phasing in the refundable CTC with the number of children: Rather than a flat 15% phase-in rate, the CTC would phase in at 15% times the number of qualifying children.

-

Allowing prior years’ income to count toward the CTC calculation: Guggenheim did not provide further detail on this provision, nor is PolicyEngine currently equipped to model it, given we use cross-sectional survey and tax data for our projections.

As the TCJA is set to expire after 2025, including its CTC expansion provisions, it is unclear what this proposal would do beyond 2025, so we constrain our analysis to 2023–2025, and focus on 2023 for illustrative examples.

Impact on a Household#

Shortly after Guggenheim reported the reform, Sharon Parrott, President of the

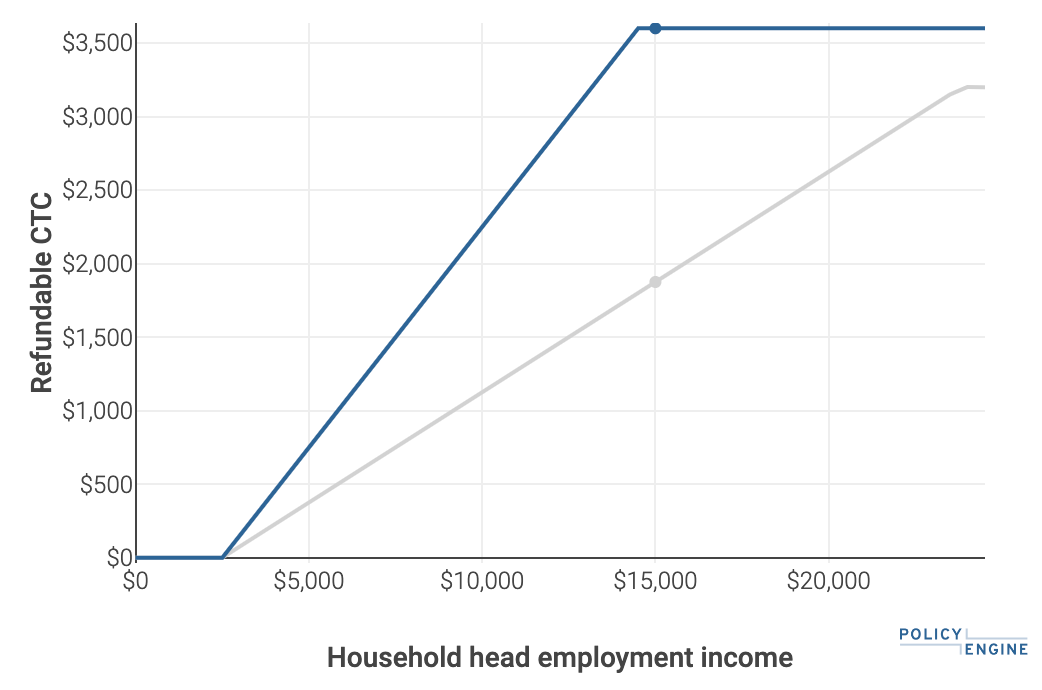

Figure 1: Refundable Child Tax Credit with respect to earnings for a single parent of two children, under current law and the Wyden-Smith reform proposal.

This earnings level is where nearly the peak benefit occurs for this family: if they earned $14,500, they would gain a full $1,800. They will benefit if their earnings range from $2,500 to $29,000.

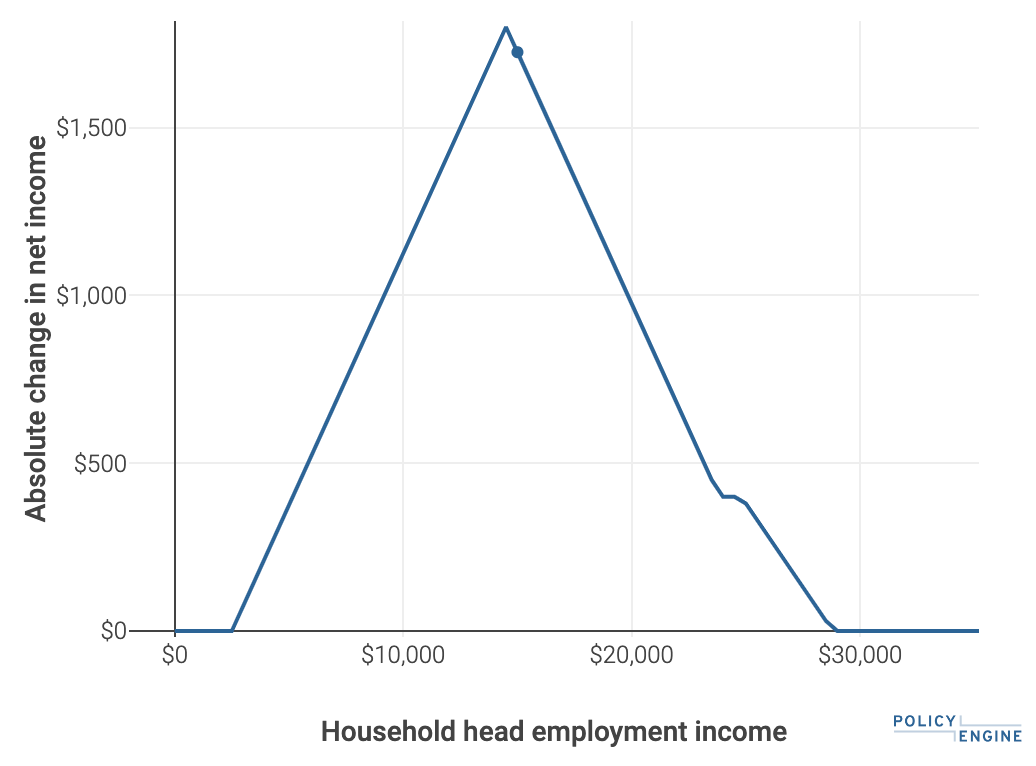

Figure 2: Impact of Wyden-Smith Child Tax Credit reform proposal on the net income of a single parent of two children.

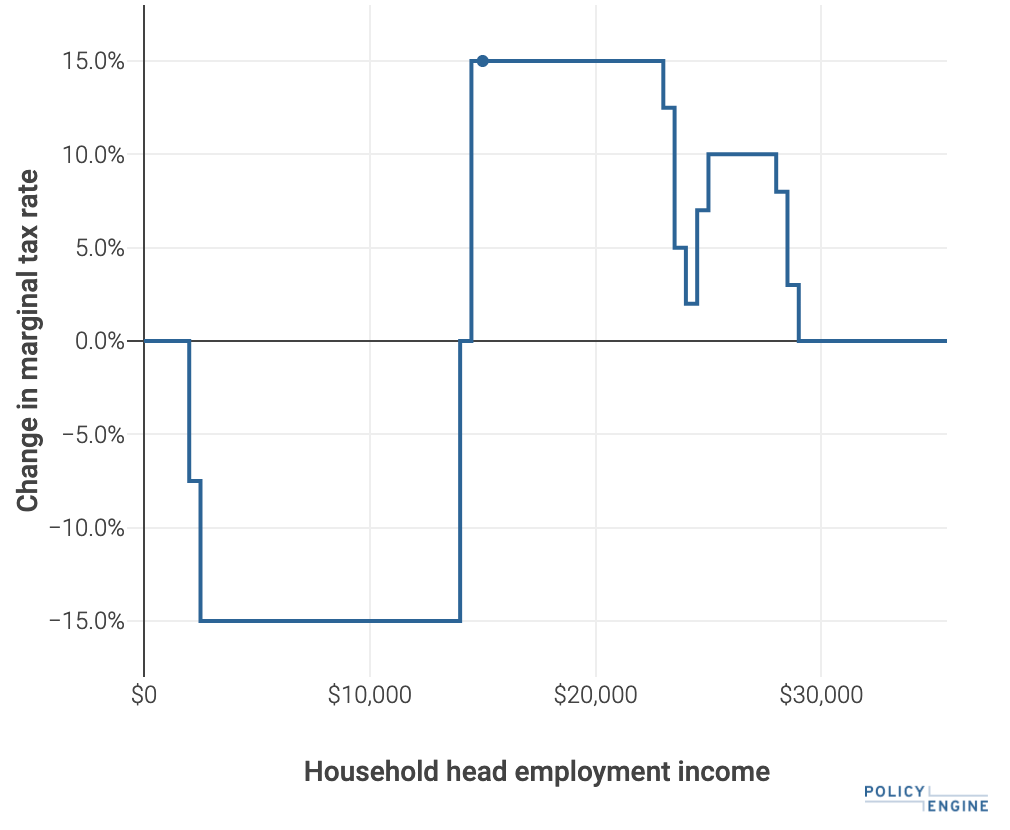

The reform would lower the household’s marginal tax rate by 15 percentage points where the ACTC phases in faster, then raise it by 15 percentage points where it stabilizes instead of previously continuing to phase in, then raise it by 10 percentage points where it begins to interact with the non-refundable CTC.

Figure 3: Impact of Wyden-Smith Child Tax Credit reform proposal on the marginal tax rates of a single parent of two children.

Societal Impact#

Applying our static tax-benefit microsimulation model over the 2022 Current Population Survey, we estimate that these two provisions would cost $5.1 billion in 2023, $5.5 billion in 2024, and $5.9 billion in 2024, for a total three-year cost of $16.4 billion.

Breaking this down between the provisions reveals that they amplify each other: summed separately, they total $4.1 billion, but together they cost $5.1 billion, since the faster phase-in rate goes further when the maximum is higher.

Table 1: Cost of Wyden-Smith Child Tax Credit reform by provision and year.

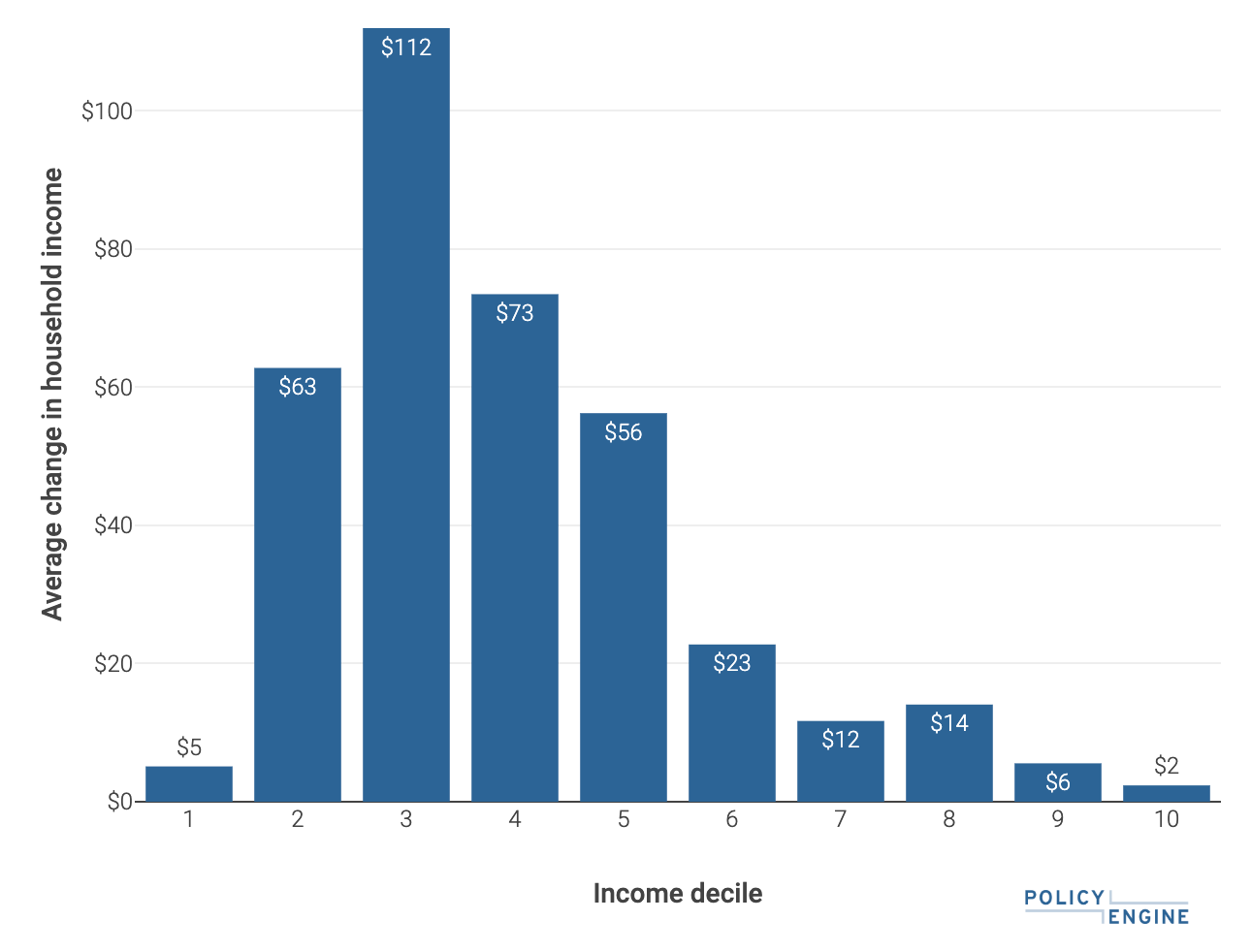

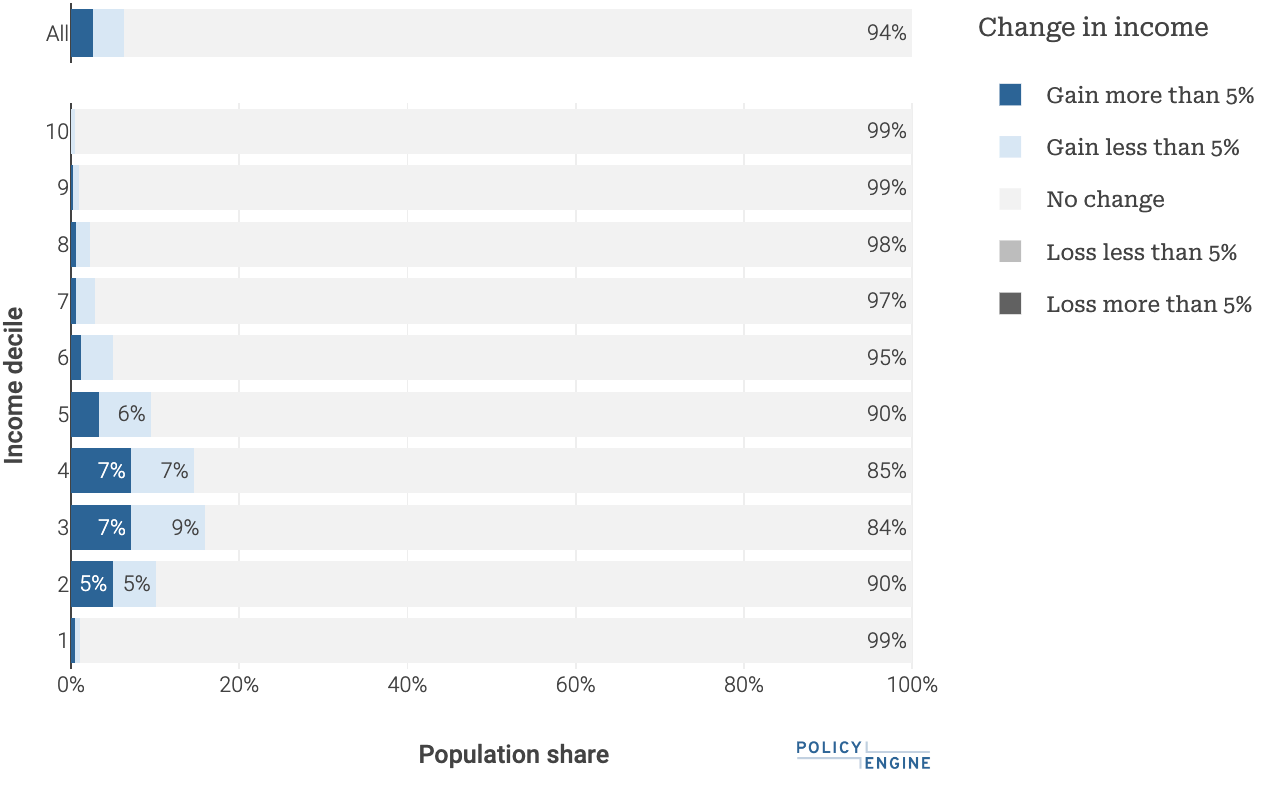

Households in the third income decile benefit most on both an

Figure 4: Impact of Wyden-Smith Child Tax Credit reform proposal by income decile.

These provisions

Figure 5: Population share gaining from Wyden-Smith Child Tax Credit reform proposal by income decile.

The number of people with resources below the poverty line would fall 1.3%, disproportionately

Results are similar in 2024 and 2025, with child poverty falling by 3.8% or 3.9%, rather than 4.3%.

Conclusion#

Wyden and Smith have proposed a three-part expansion to the Child Tax Credit, of which PolicyEngine can currently model two. Firstly, it raises the maximum refundable ACTC amount incrementally from 2023 to 2025; secondly, it modifies the phase-in rate of the refundable CTC to be a function of the number of qualifying children; and thirdly, it includes a provision to allow the CTC calculation to be based on prior years’ income, a feature not currently supported.

The estimated impacts of the first two provisions on households include adjustments in the Child Tax Credit received at various income levels; for instance, a single parent of two would benefit if their earnings range from $2,500 to $29,000. These changes also influence marginal tax rates due to the modified phase-in rate of the ACTC.

From 2023 to 2025, the first two provisions would cost $16.4 billion, cut child poverty about 4%, benefit about 6% of Americans, and reduce deep poverty and income inequality. These impacts are relatively stable across the three years, and we do not project further due to the expiration of the Tax Cuts and Jobs Act after 2025.

As negotiations proceed, we will continue to develop our software platform to support a range of Child Tax Credit analyses, including those like the third provision to base the credit on prior years’ income (which also require further definition). Stay tuned and

max ghenis

PolicyEngine's Co-founder and CEO

pavel makarchuk

Economist at PolicyEngine

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

© 2025 PolicyEngine. All rights reserved.