Analysing Autumn Budget Universal Credit reforms with PolicyEngine

See how the reform affects the UK population or your household.

Contents

How Universal Credit works

The maximum rate

Reductions from income

Analysis

UK impact

Household impact

Entitlement

Marginal tax rates

Chancellor of the Exchequer Rishi Sunak. Credit:

On Wednesday, the UK’s Chancellor of the Exchequer Rishi Sunak

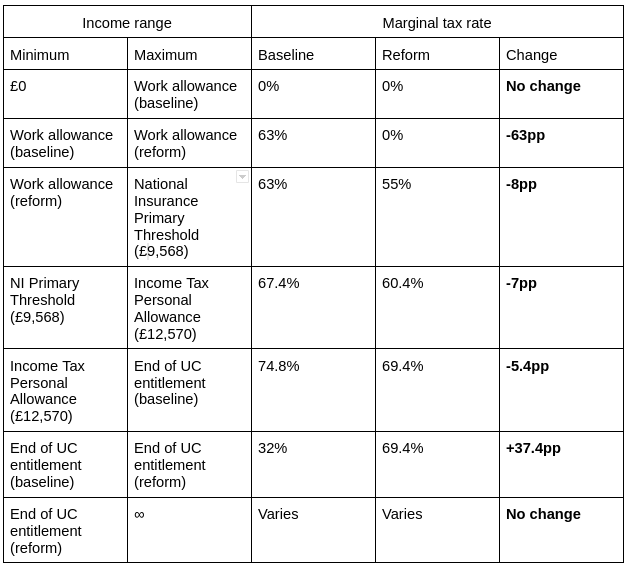

PolicyEngine estimates that this reform would cost £2.8bn per year, reduce poverty by 3.1%, and benefit 12% of the population. It will also reduce marginal tax rates by between 5.4pp and 63pp for people with income between the baseline work allowance and UC entitlement, while raising marginal tax rates by 37.4pp for people with income previously too high to receive UC.

Read on for more details, or

How Universal Credit works#

Universal Credit is the central in-work means-tested benefit, currently being rolled out across the UK. The benefit replaces six existing “legacy” benefits covering unemployment, limited work capability and low earnings. The roll-out was started in 2013 and

The maximum rate#

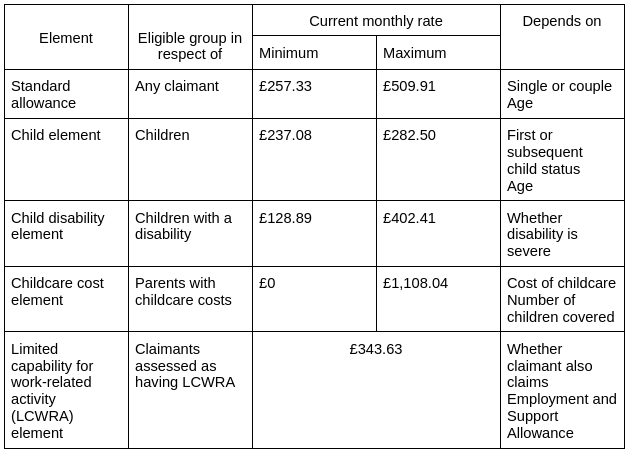

Universal Credit payments are paid in respect of a benefit unit (one or two cohabiting adults, plus children). Entitlements are calculated based on three steps: the first, eligibility, requires that the claimant be working-age. The second step calculates the maximum entitlement, by summing any of the following elements that apply.

Values of components in Universal Credit, as of 28th October 2021.

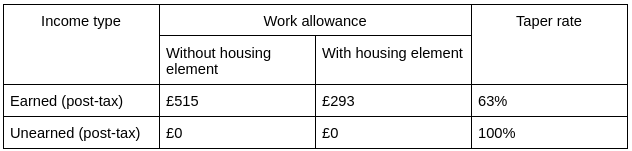

Reductions from income#

Income received by the claimant reduces their entitlement to Universal Credit. Unearned income (other benefits, pensions and capital income) is treated differently than earned income from employment or self-employment. Income, after deducting taxes and work allowances, reduces UC entitlement in proportion to the taper rate.

The means test parameters of Universal Credit, as of 30th October 2021.

Analysis#

The reforms announced in the budget reduce the taper rate by 8pp, from 63% to 55%, as well as increasing both work allowances by £50 per month. This increases entitlement for those with earnings, in proportion to their earnings, and smoothens marginal tax rates.

UK impact#

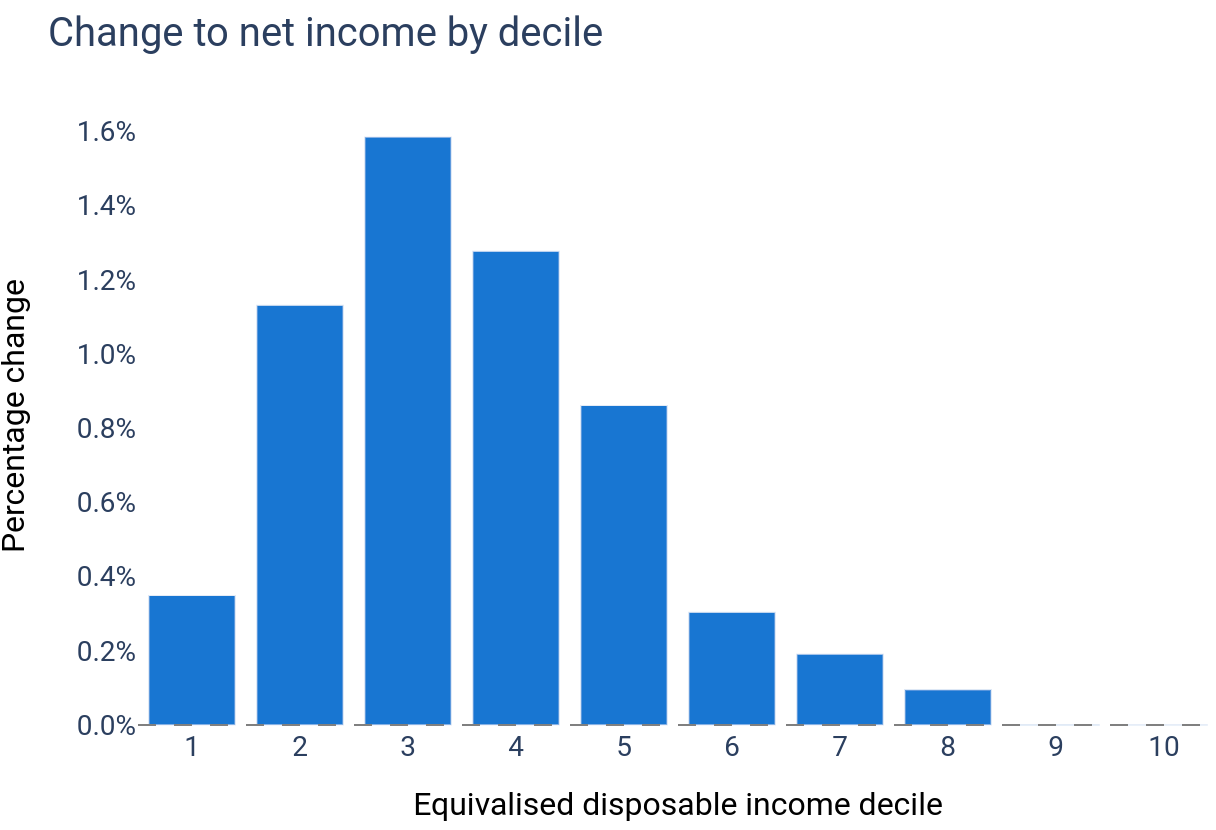

PolicyEngine estimates the total cost of introducing the reform to be £2.7bn per year. The reform benefits 12% of the population, and it reduces poverty by 3.1% (working-age poverty decreases by 3.0% and child poverty by 6.0%). For context, PolicyEngine estimates that

Broadly, the reform is progressive; however, individuals in the first decile gain less than those in the second, third and fourth deciles, due to their lower likelihood to earn above the Work Allowance.

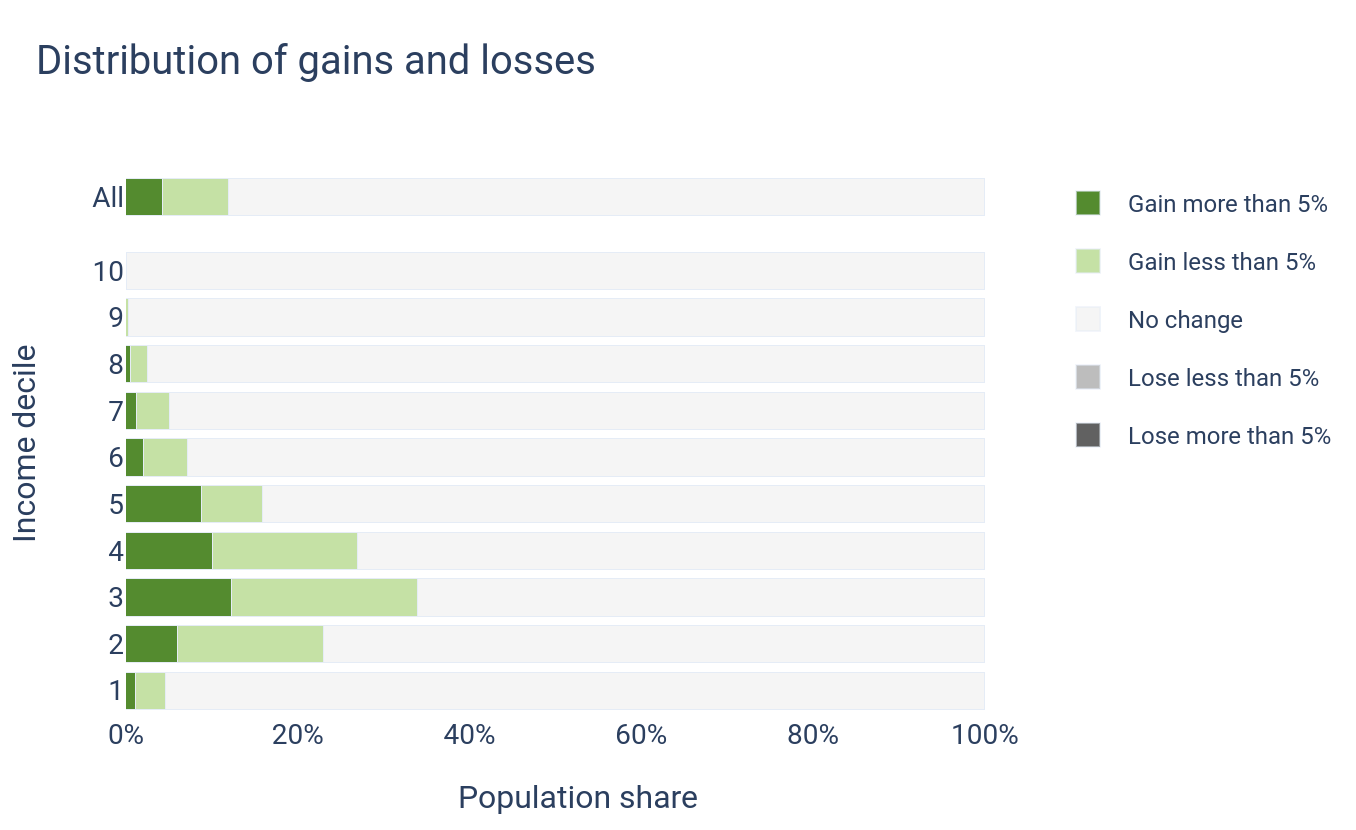

Around a third of those affected see an increase in their disposable income of more than 5%. This reform targets those in the third income decile, with those in the first decile targeted around as much as those in the seventh.

Household impact#

Entitlement#

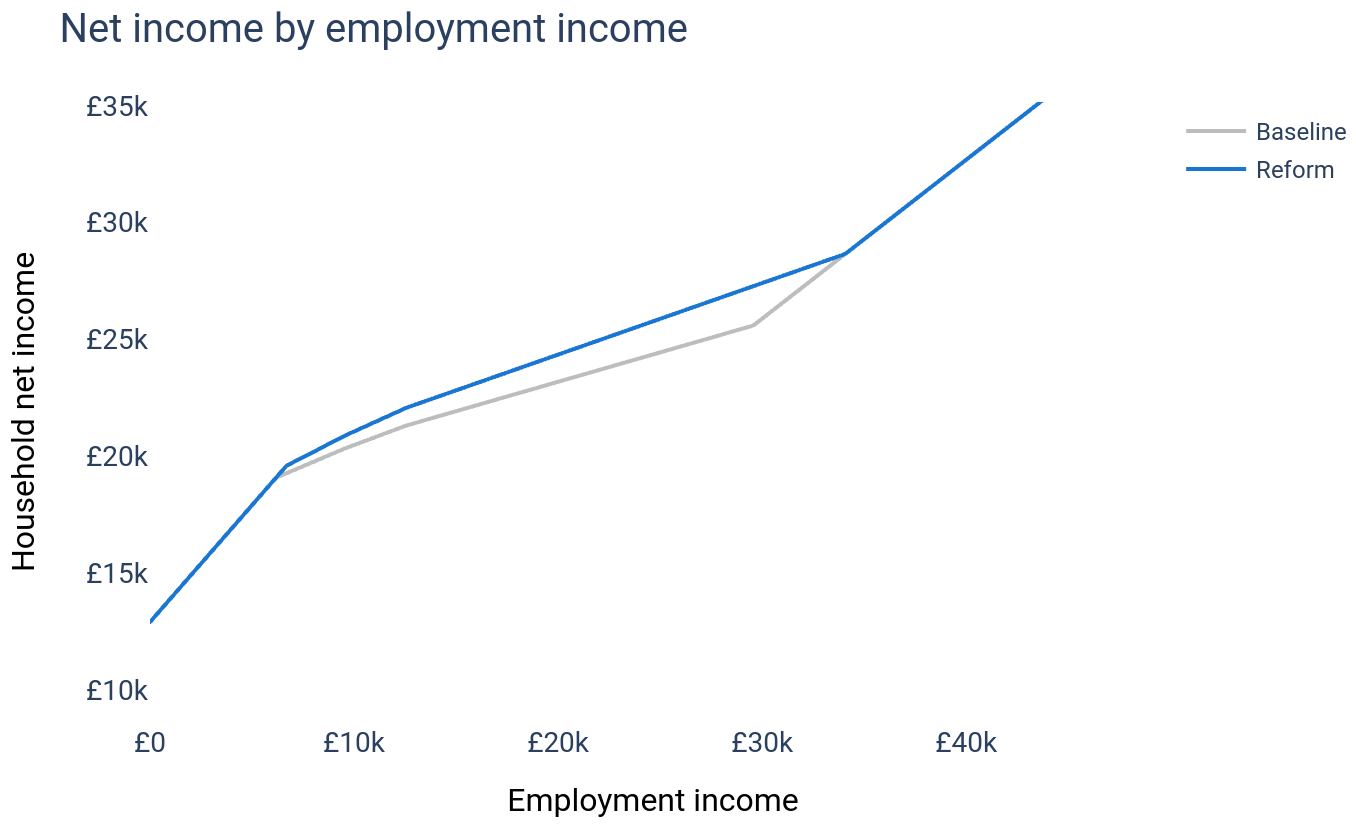

This reform excludes unpaid and very-low-paid claimants from any gains, unlike the pandemic-related increases to the standard allowance, as those with earnings under the baseline Work Allowance will be unaffected by changes to the taper rate or allowance. As shown below, the increases to disposable income begin at the baseline work allowance, increase with earnings, and end once UC entitlement reaches zero.

How the reform affects net income for a non-renting two-adult, two-child household.

Marginal tax rates#

The marginal tax rate is the share of an additional pound of income that the government takes, through either taxation or benefit withdrawal. The reform reduces marginal tax rates in the main, but marginal tax rates will increase for some. The table below outlines the circumstances where marginal taxes will change.¹

How the UC reform affects marginal tax rates.

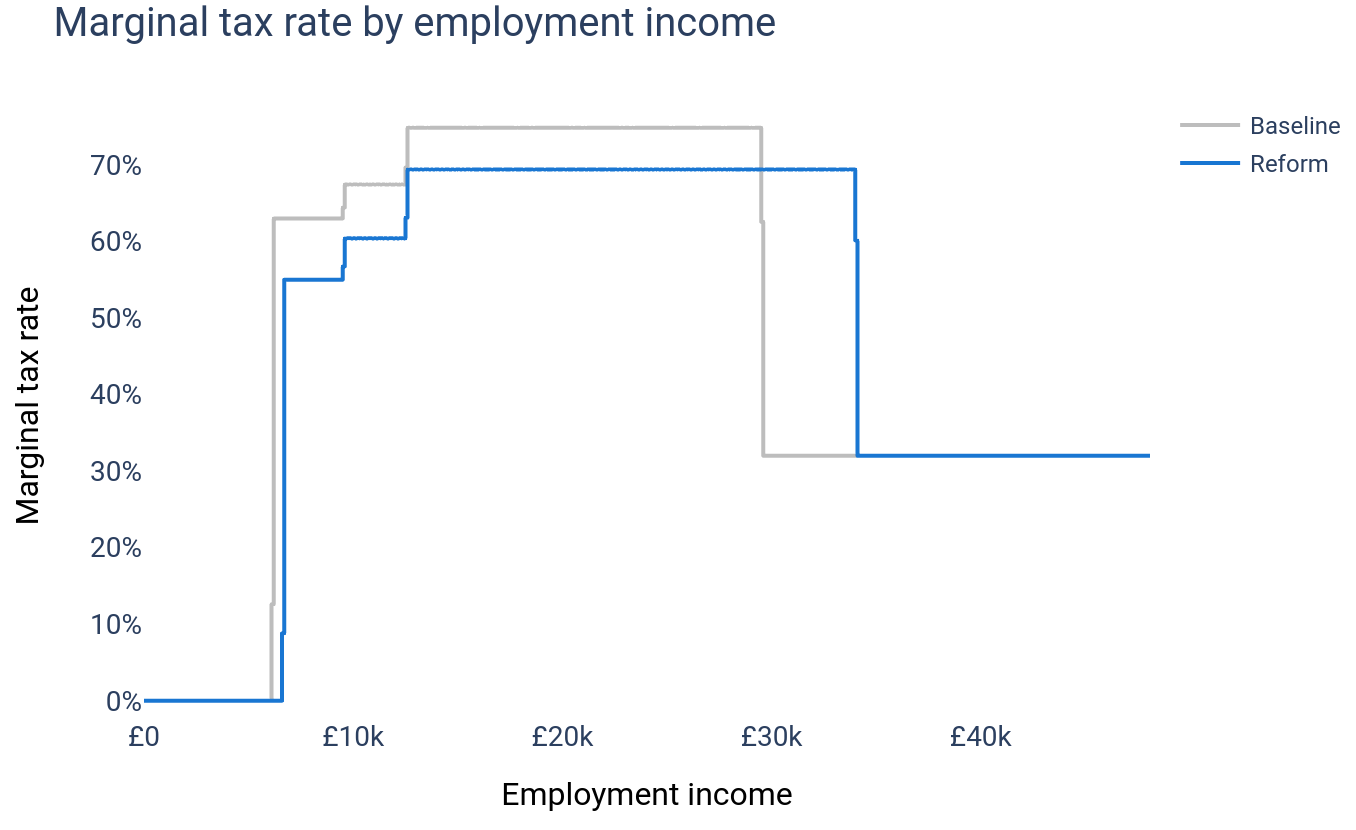

A couple with two children and no rental costs will see their marginal tax rate fall if they earn between £6,180 and £32,540, and rise if they earn between £29,400 and £37,460, where they would be newly eligible for UC.

How the reform affects marginal tax rates for a non-renting two-adult two-child household.

The reform lowers marginal tax rates more than it raises them, but its effect is reduced by Income Tax and National Insurance. Furthermore, the family is affected for longer by the taper rate, which is several times larger than any other marginal tax.

We’re pleased to share this first interactive analysis of the Autumn Budget UC reform, and the first to provide personalised household impacts. Our findings broadly resemble those from the

For more timely analysis of tax and benefit reforms, follow us here and on social media, and to create your own policy, try PolicyEngine at

2021–11–04 update: This now reflects PolicyEngine 1.1.0, which incorporates Universal Credit’s minimum income floor for self-employed people.

2021–11–06 update: This now reflects PolicyEngine 1.1.1, which calculates poverty consistently for the year 2021.

2021–11–15 update: This now reflects PolicyEngine 1.1.8, which projects poverty thresholds and population to 2021.

[1]: Other programs, like the Child Benefit High-Income Tax Charge, can interact with Universal Credit to produce different results depending on household composition.

nikhil woodruff

PolicyEngine's Co-founder and CTO

Subscribe to PolicyEngine

Get the latests posts delivered right to your inbox.

PolicyEngine is a registered charity with the Charity Commission of England and Wales (no. 1210532) and as a private company limited by guarantee with Companies House (no. 15023806).

© 2025 PolicyEngine. All rights reserved.